WWhat do I get when I buy this product?

A basic sole trader self assessment tax return made easy.

This product is designed to meet the HMRC requirements for self assessment for self employed sole traders. Prepared by an ACCA registered chartered accountant.

Who should buy this product?

If you are a self employed sole trader you can easily purchase and this product.

Applies only to UK registered tax payers.

It’s easy: complete an online form and we will do the rest.

At your convenience

The most convenient way to prepare your tax return.

After you have purchased this product we will forward you a form to complete and request information and accounts from you.

Based upon those replies one of our tax specialists will prepare your tax return.

No need to attend accountant’s offices, this purchase is completed online from the convenience of your office or the comfort of your home.

Price promise

Fixed price. No more unexpected, unexplained accountant’s bills.

We will prepare your tax return ready for you to file yourself or we will file it for you. If you want us to file your tax return simply add FILING to your shopping trolley when requested.

Guaranteed - NO MORE MISSED DEADLINES

If you provide us with the information in the exact format which we request it and within our specifically stated timeframes we guarantee that we will prepare your return within HMRC’s filing deadlines.

What are a Sole trader’s statutory obligations?

All self employed people (even if they have other part-time or full-time employment) have legal duty to:

1. Register with HMRC within 3 months of beginning to trade.

2. Each tax year prepare and complete a set of accounts the figures from which are used to:

3. Prepare and file an individual self assessment tax return (SA100).

1. Register with HMRC.

Each tax year prepare and file a self assessment tax return.

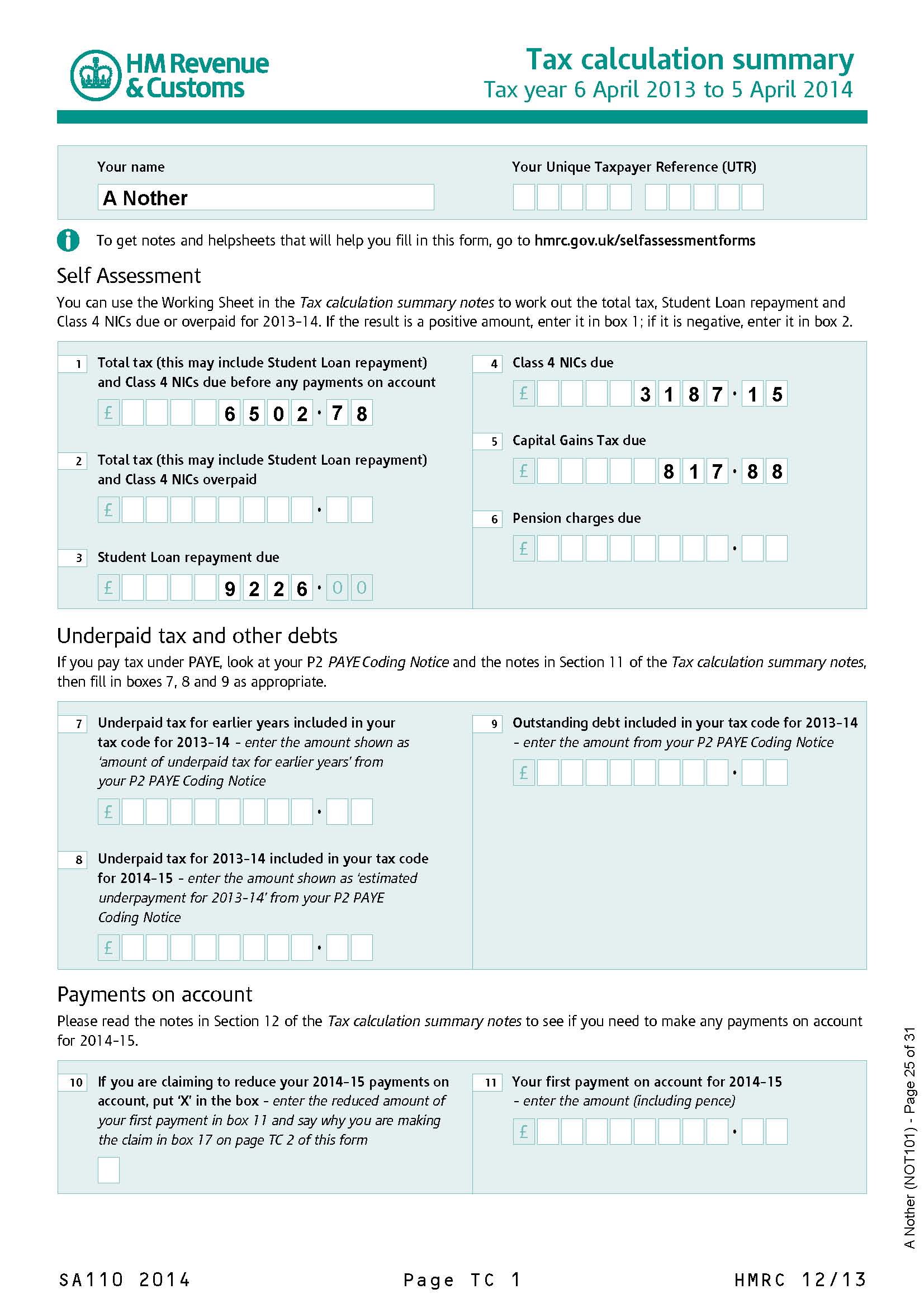

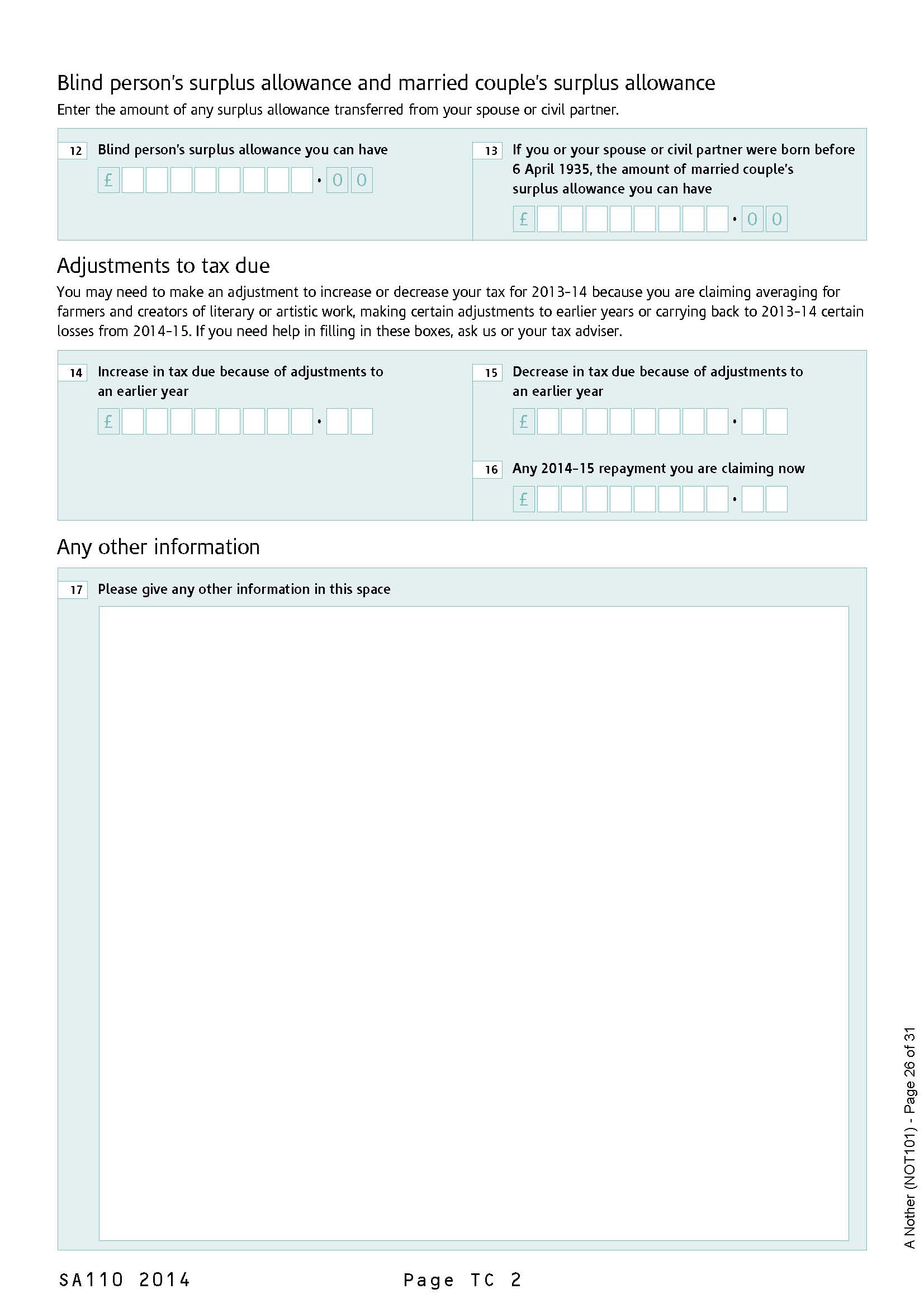

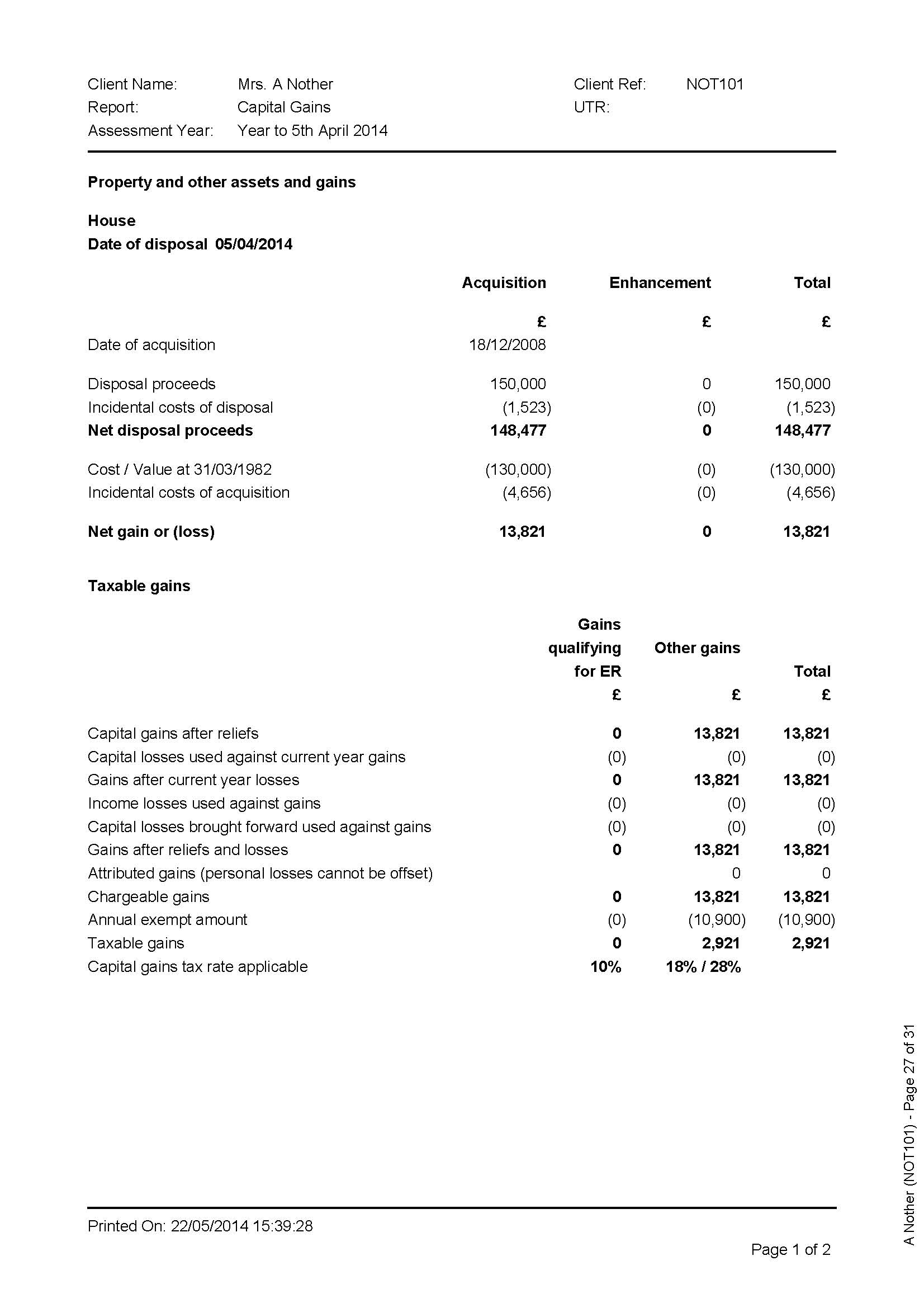

What this product includes:

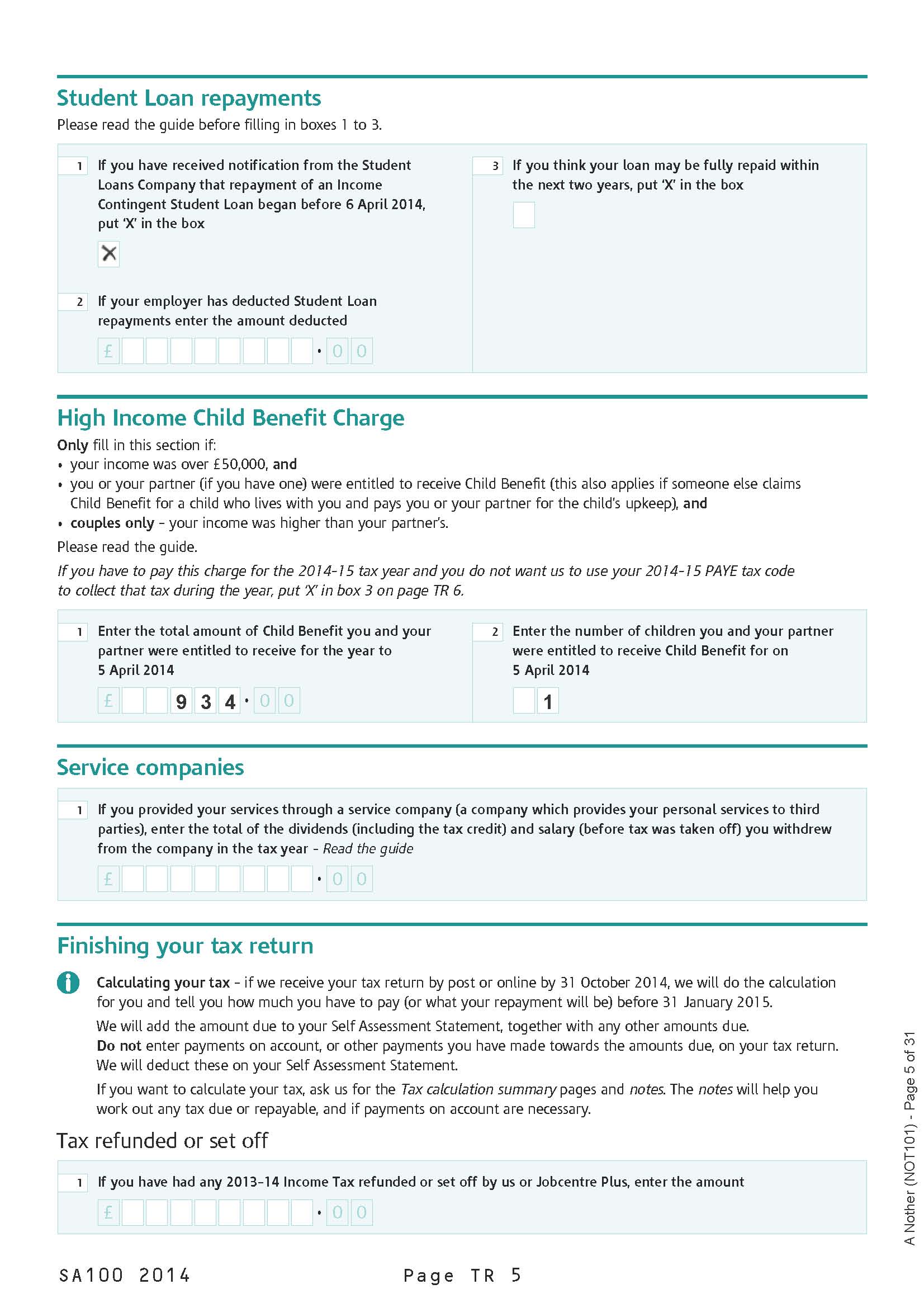

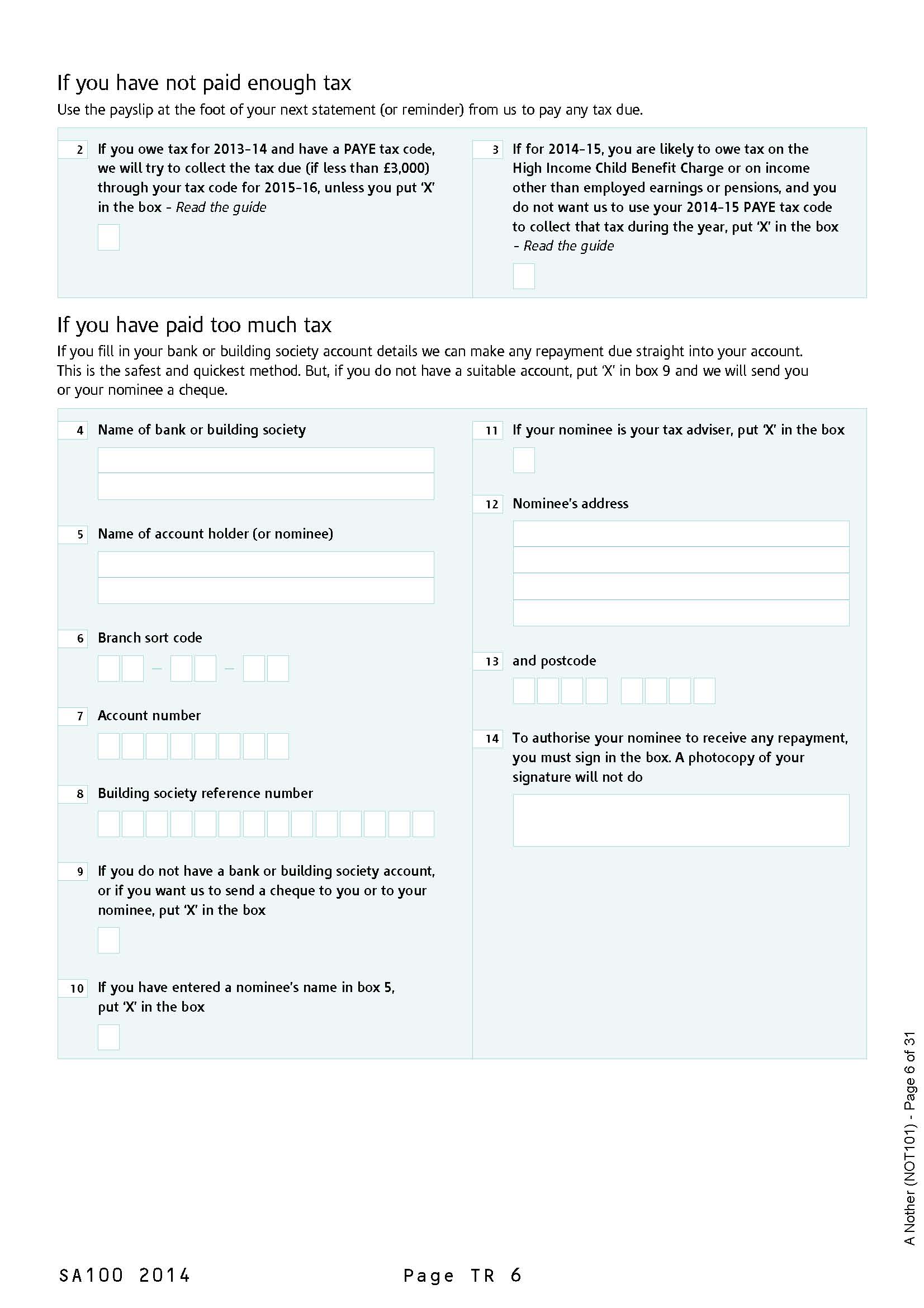

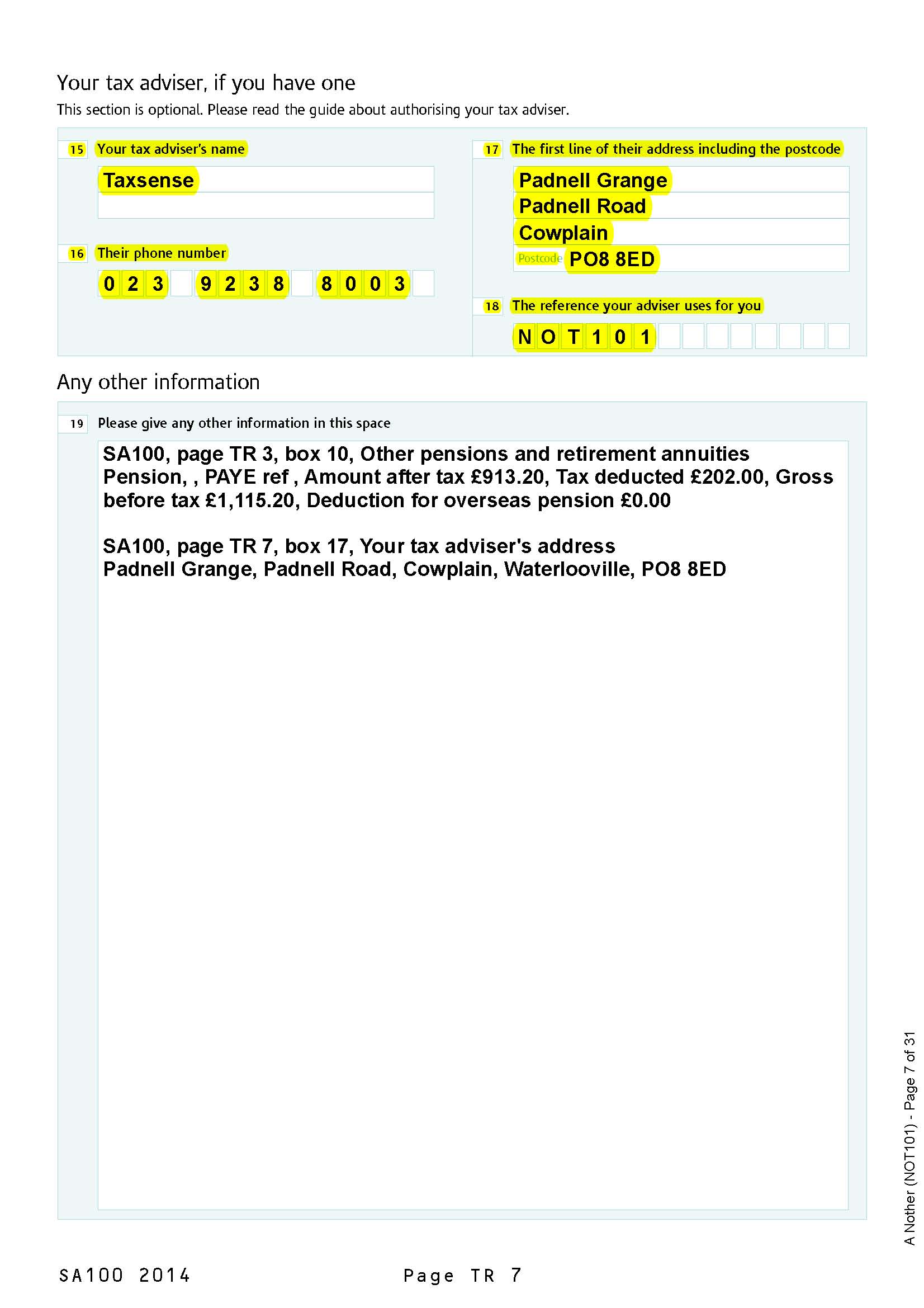

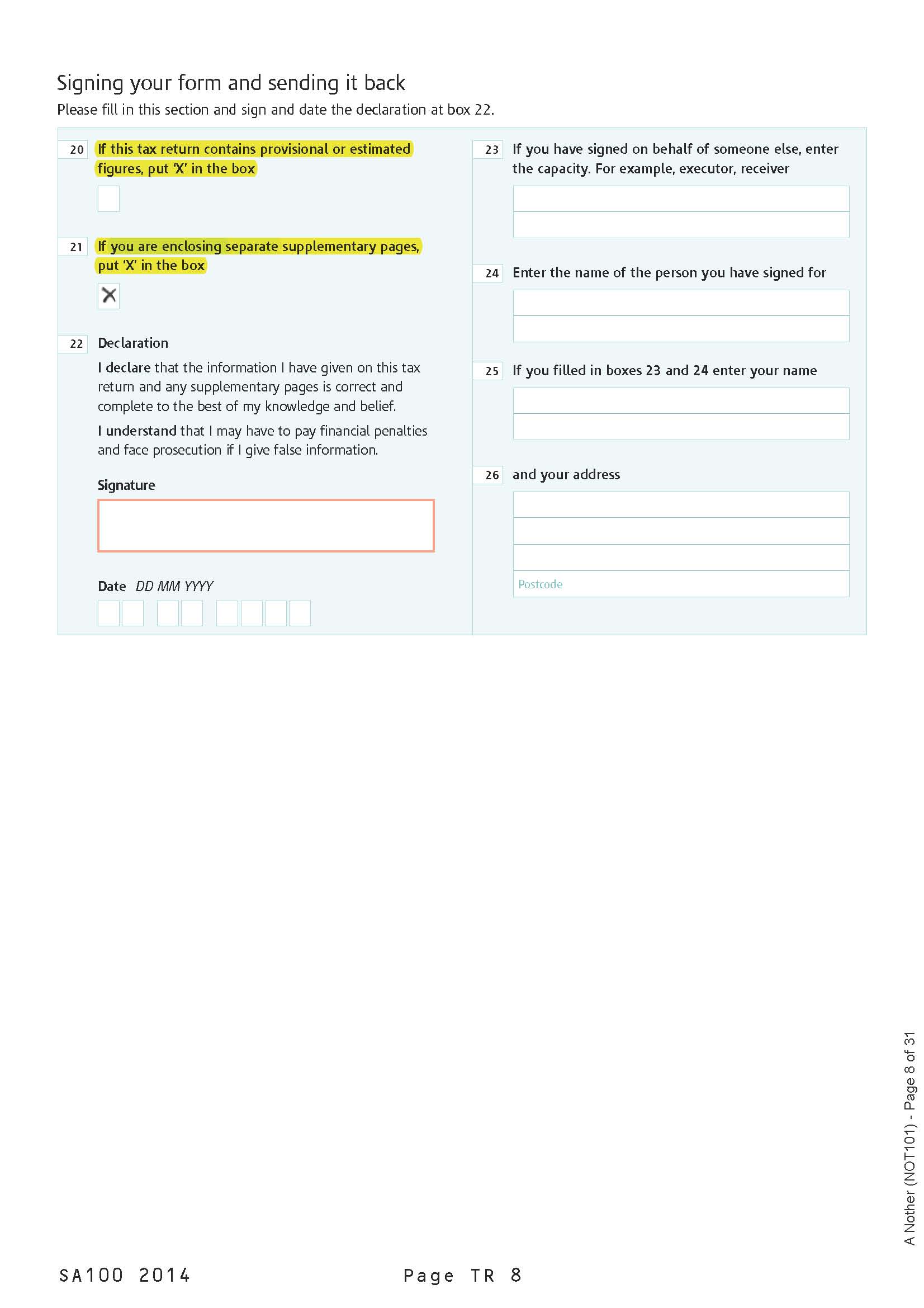

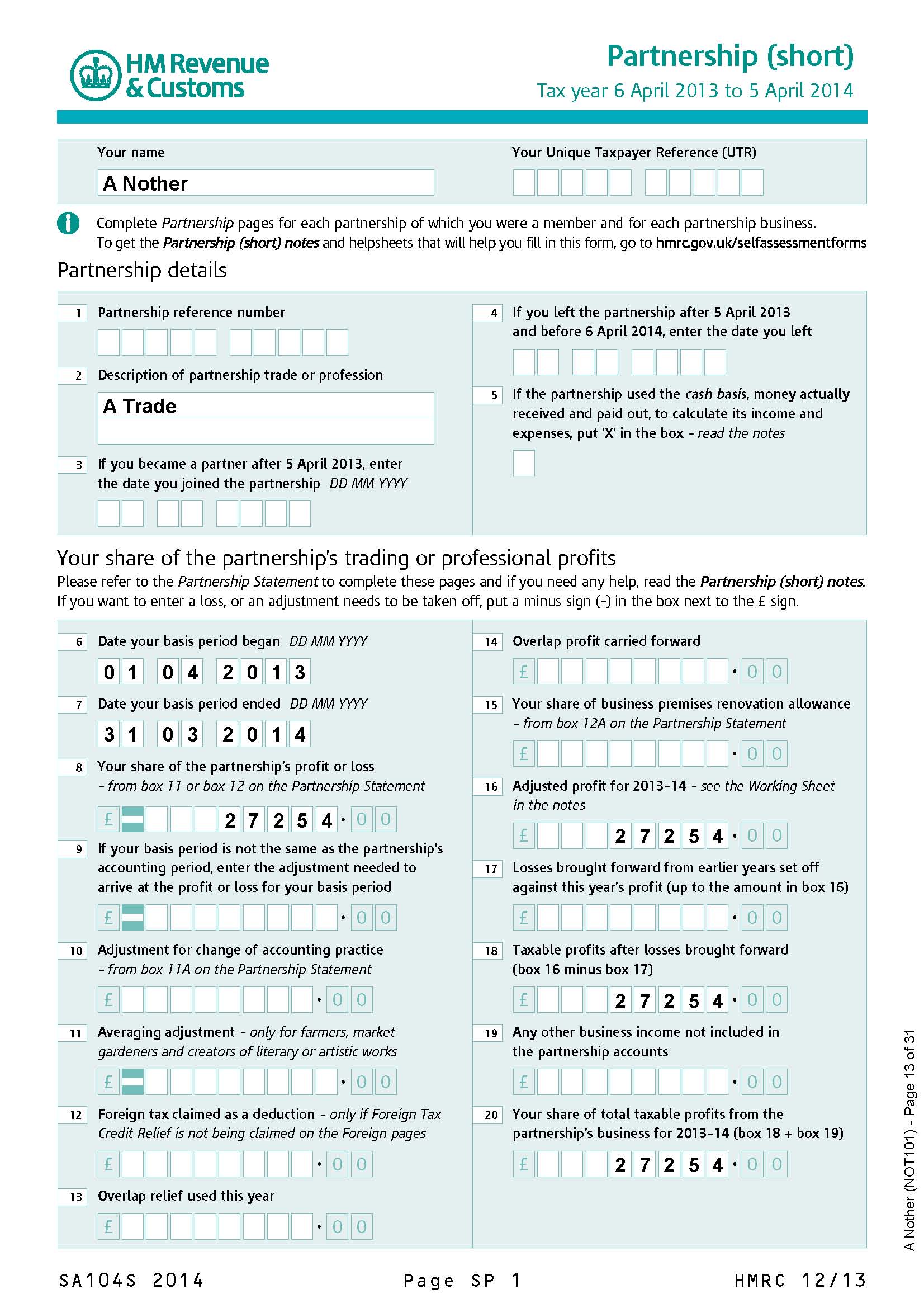

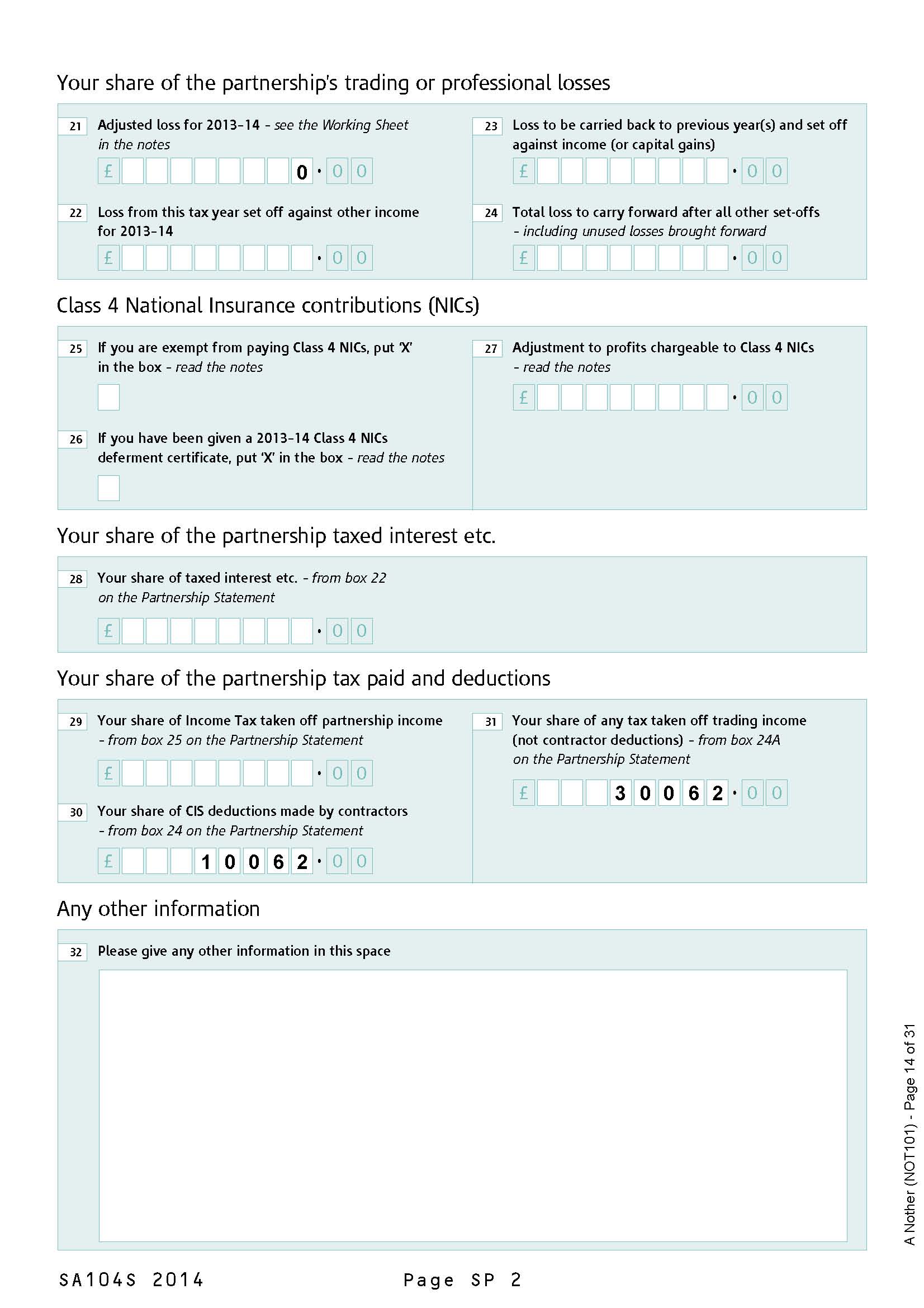

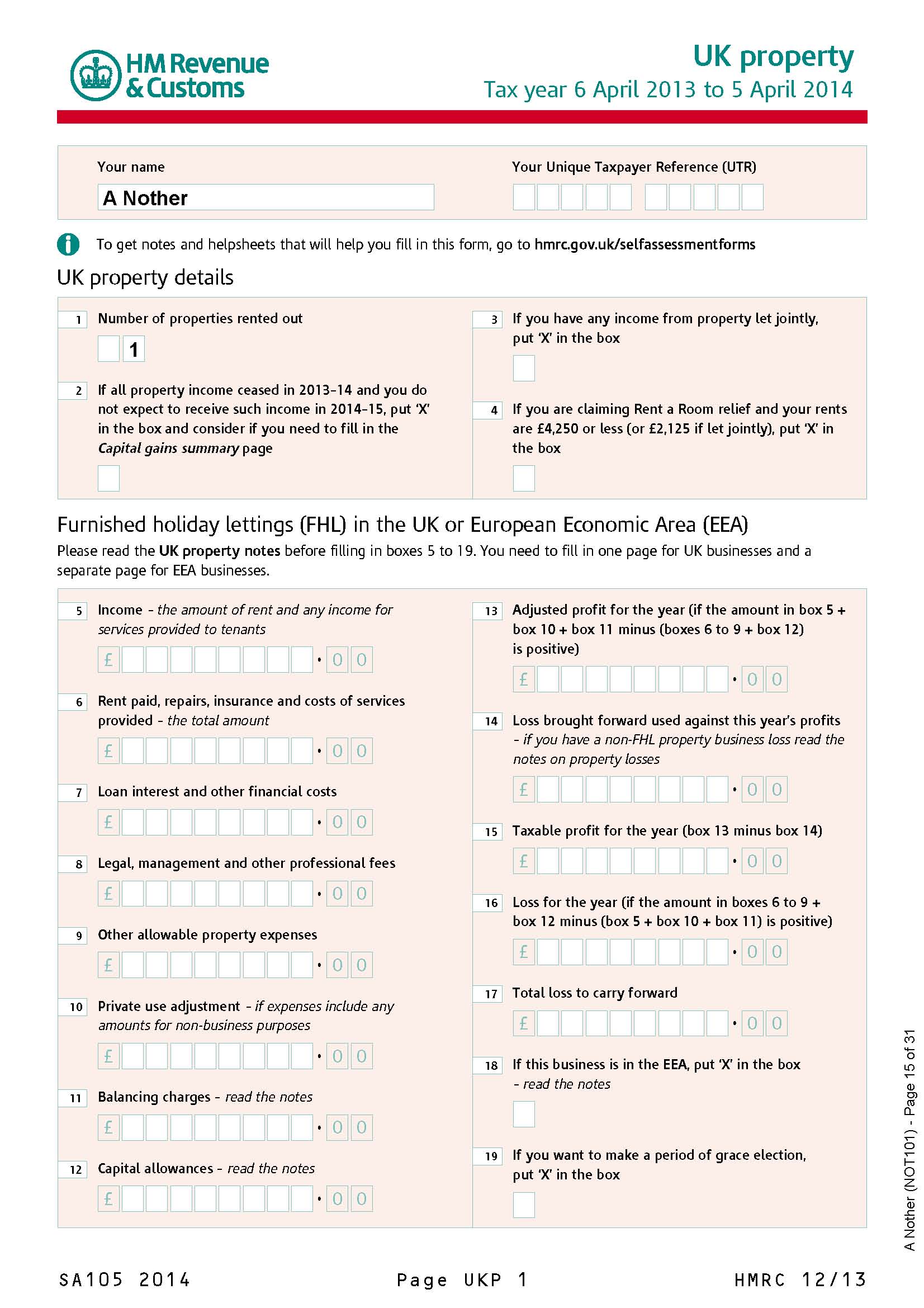

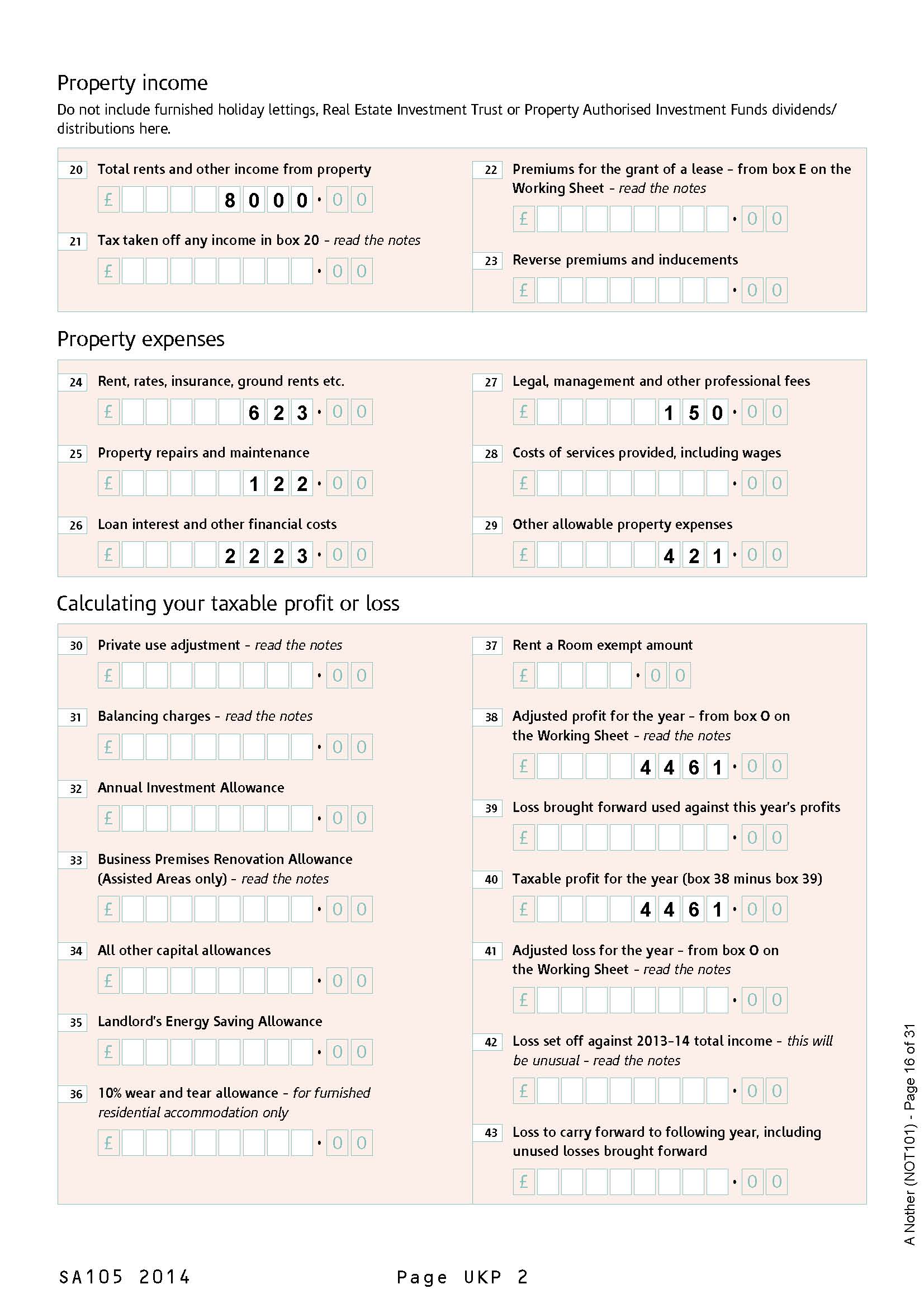

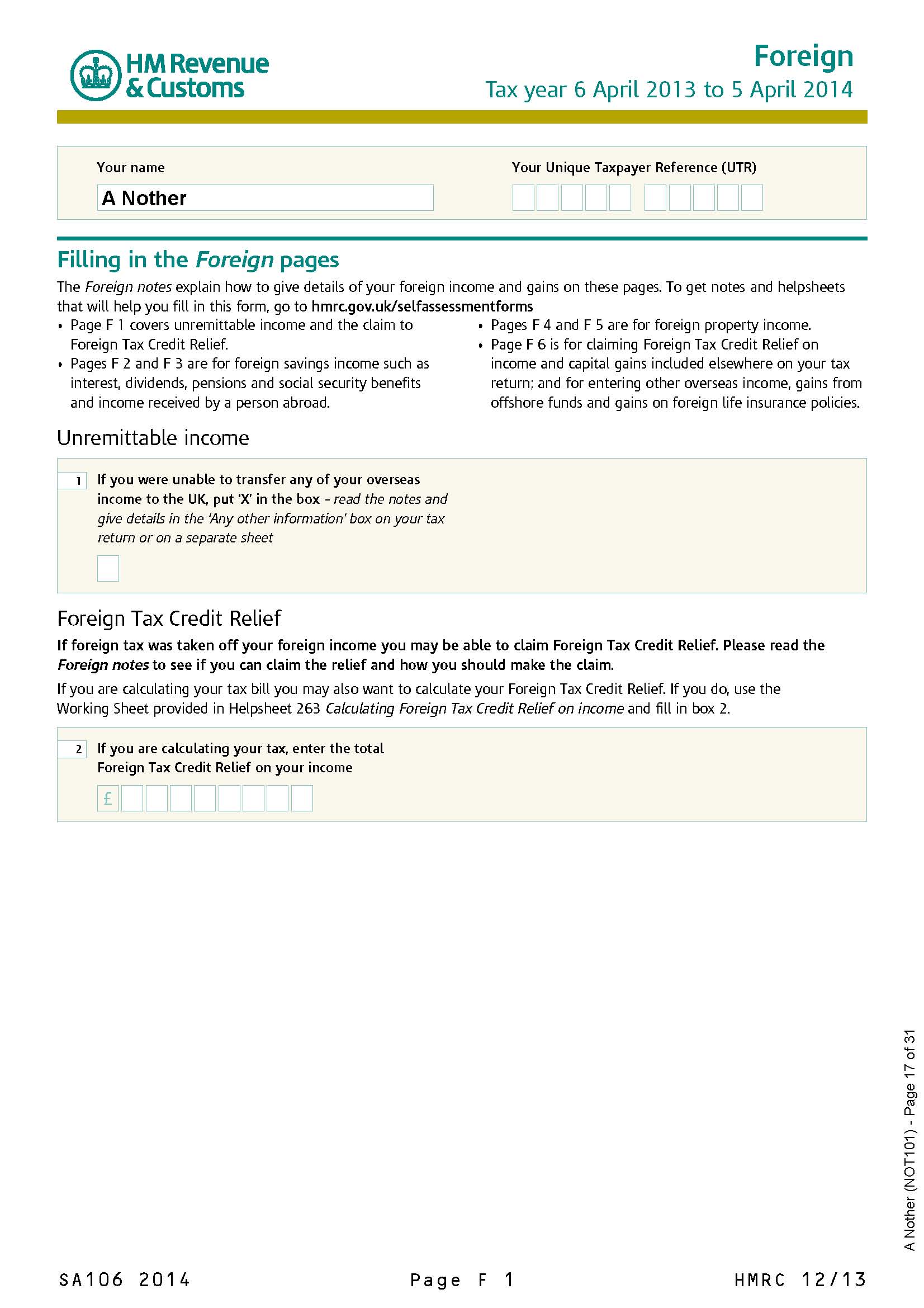

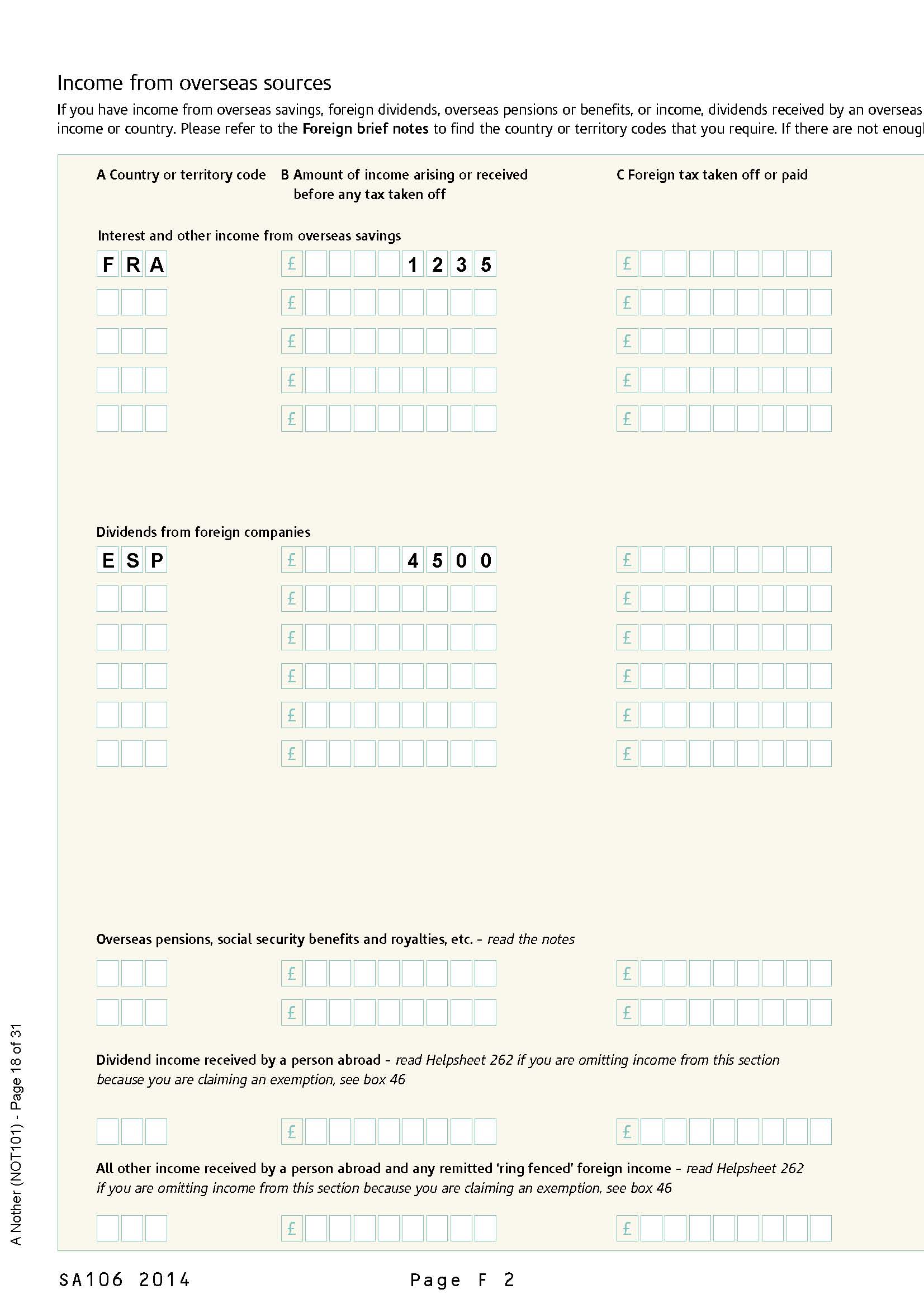

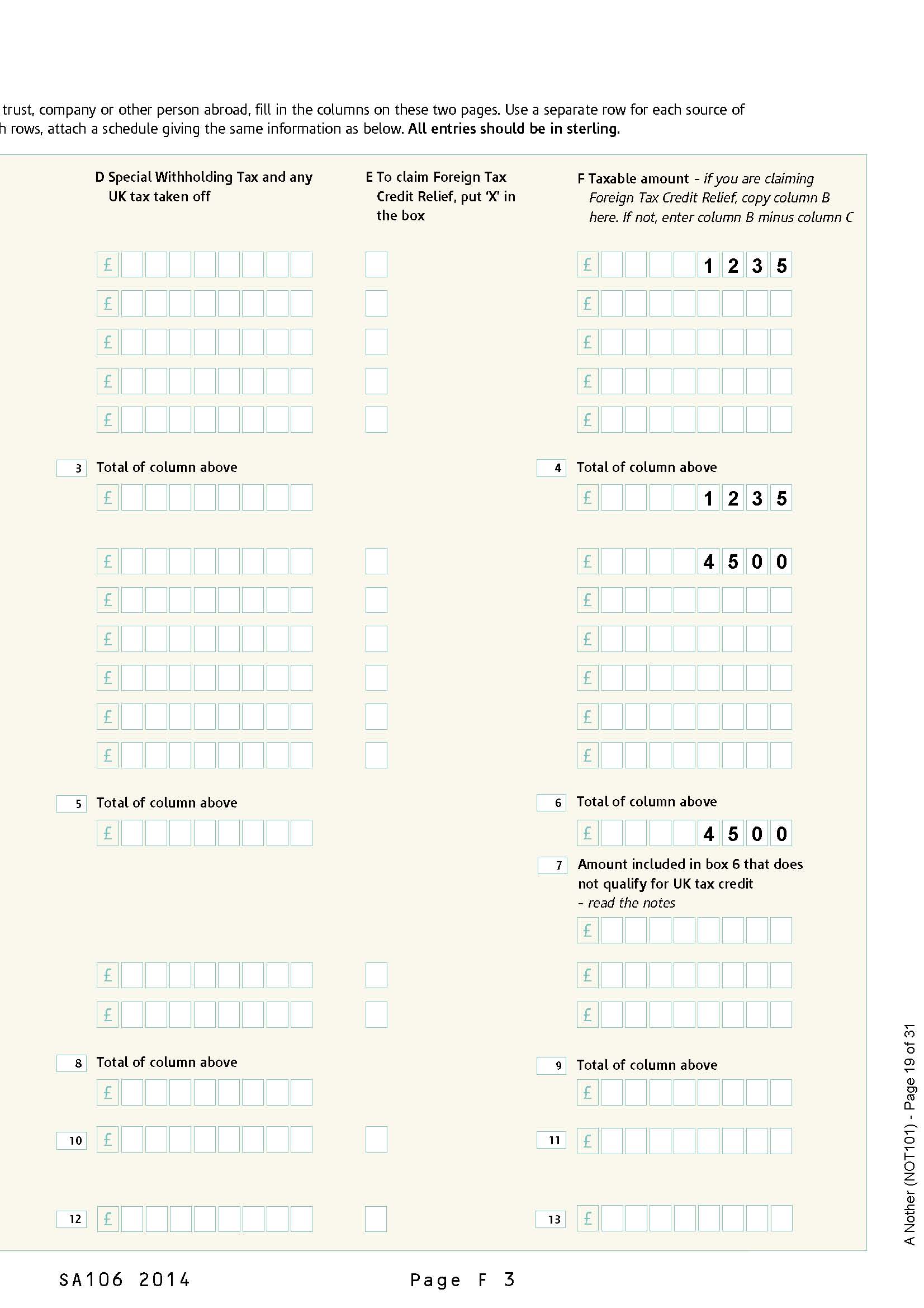

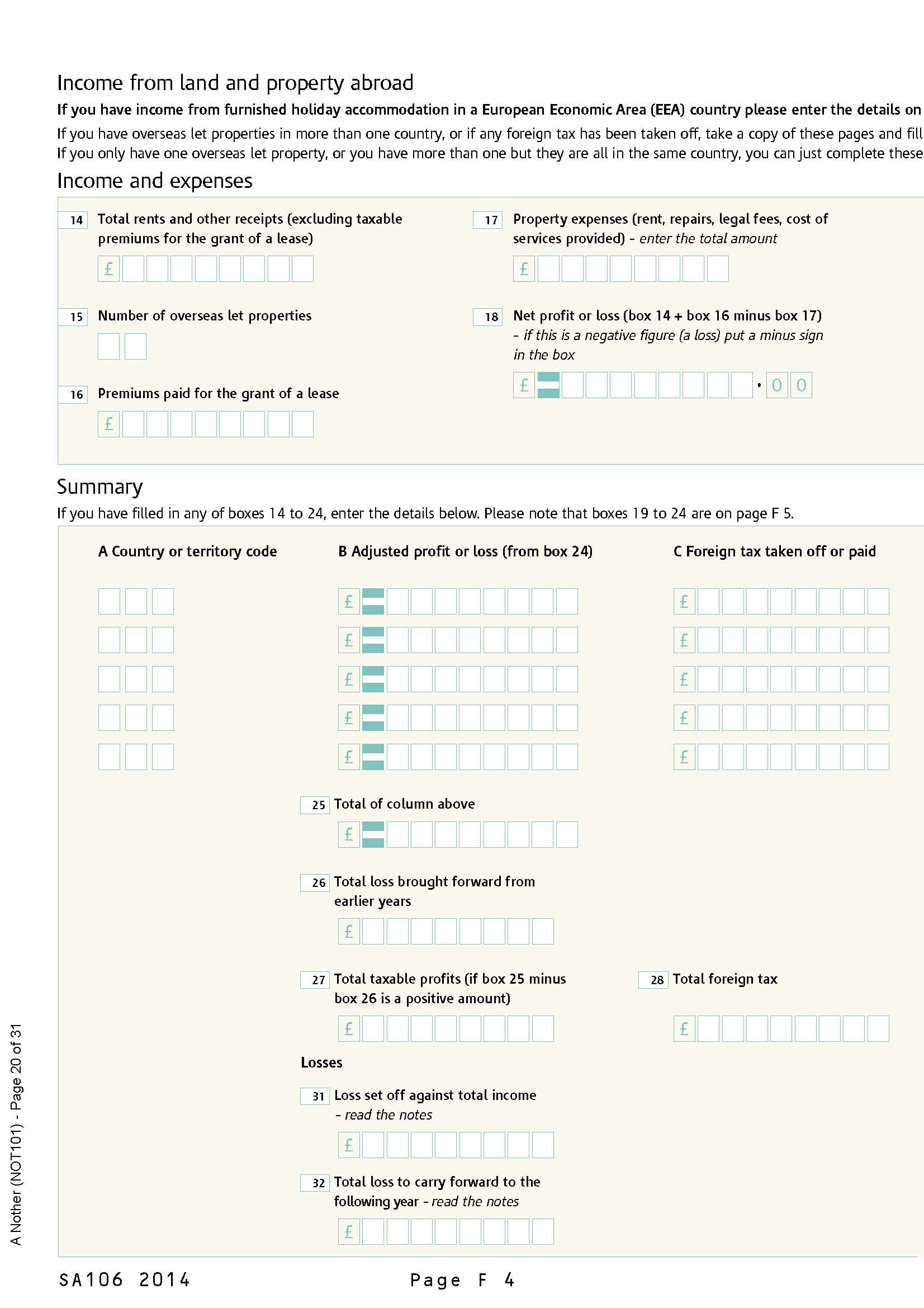

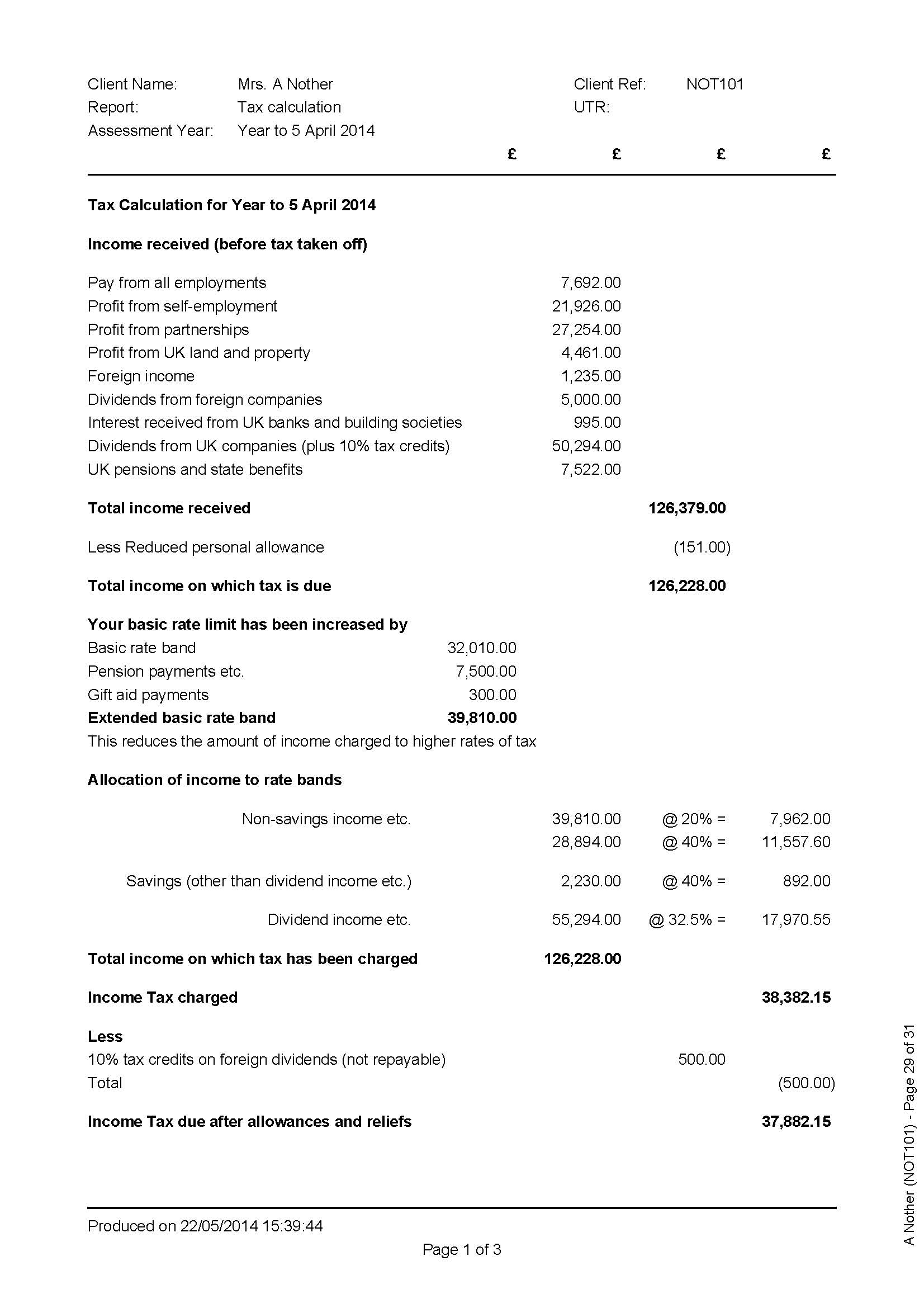

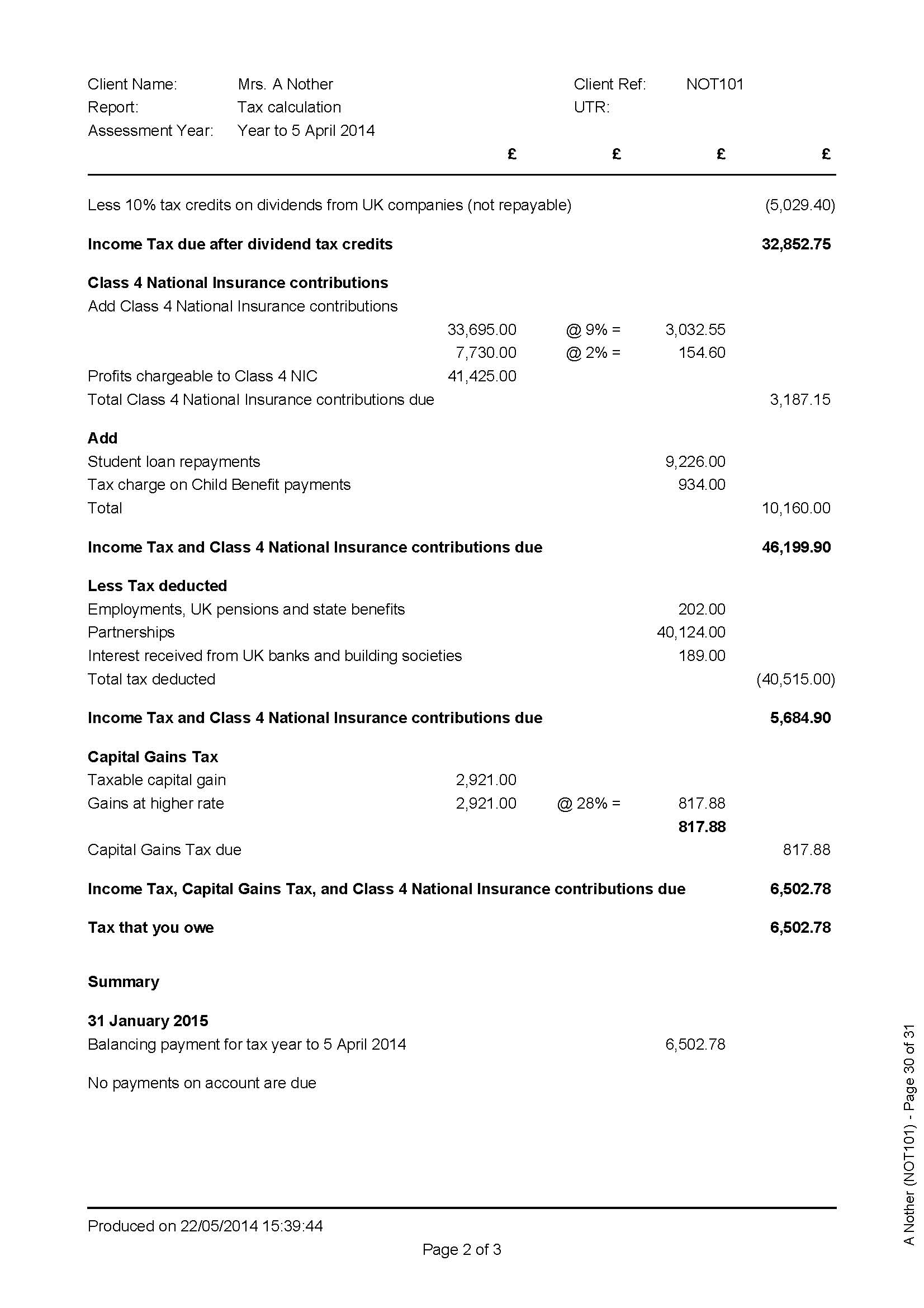

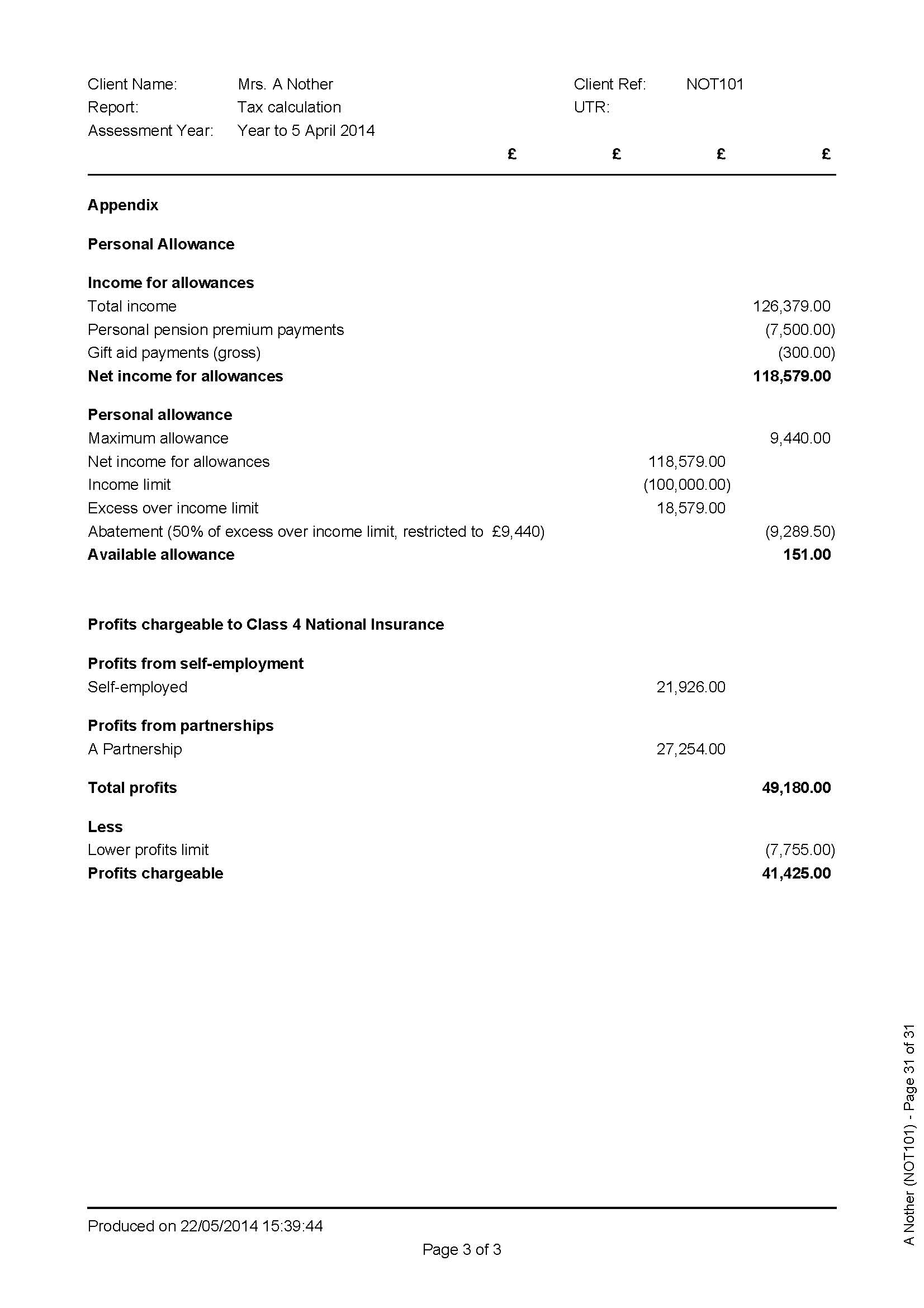

The product images show exactly which sections of a tax return are included with this product.

Every sole trader gets the basic tax return issued to them by HMRC. There are other, ‘supplementary’, pages covering the less common types of income, and disposals of chargeable assets.

If you need or think you may need any other sections, or other supplementary sections, please see ‘other sections of the tax return which may apply’ and add those to your basket. However we will contact you with a detailed questionnaire after you purchase the product to check if you have included everything you will need.

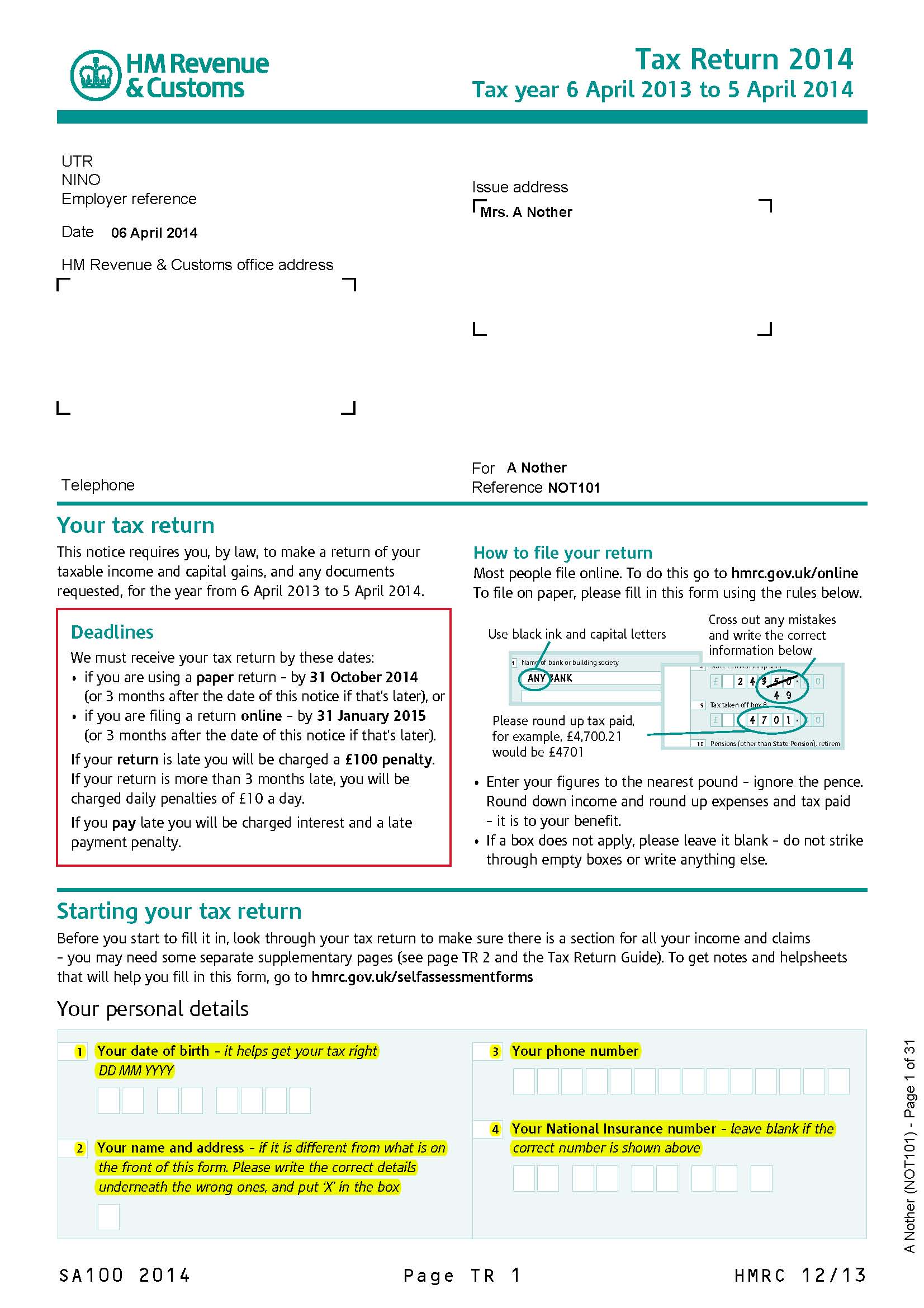

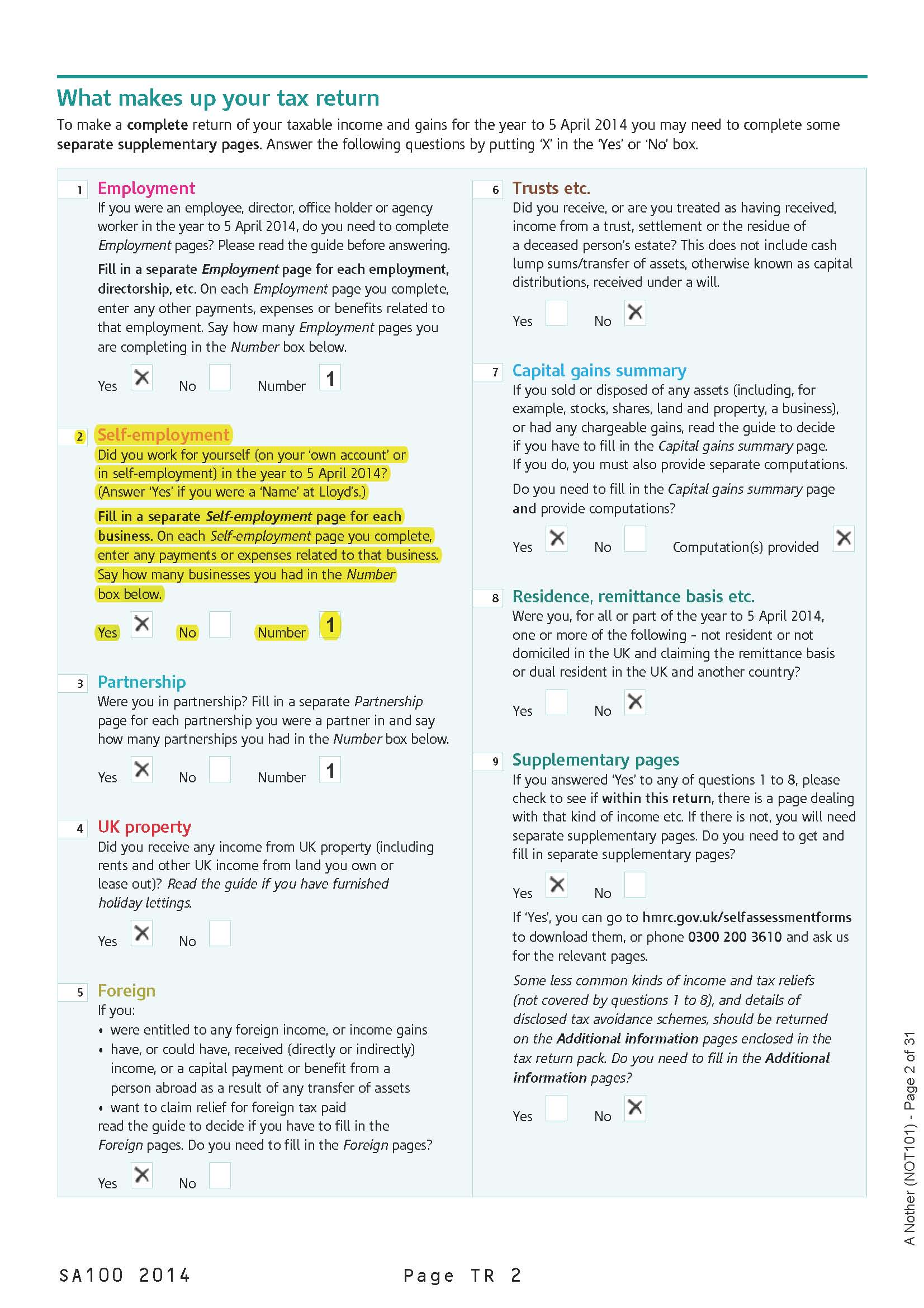

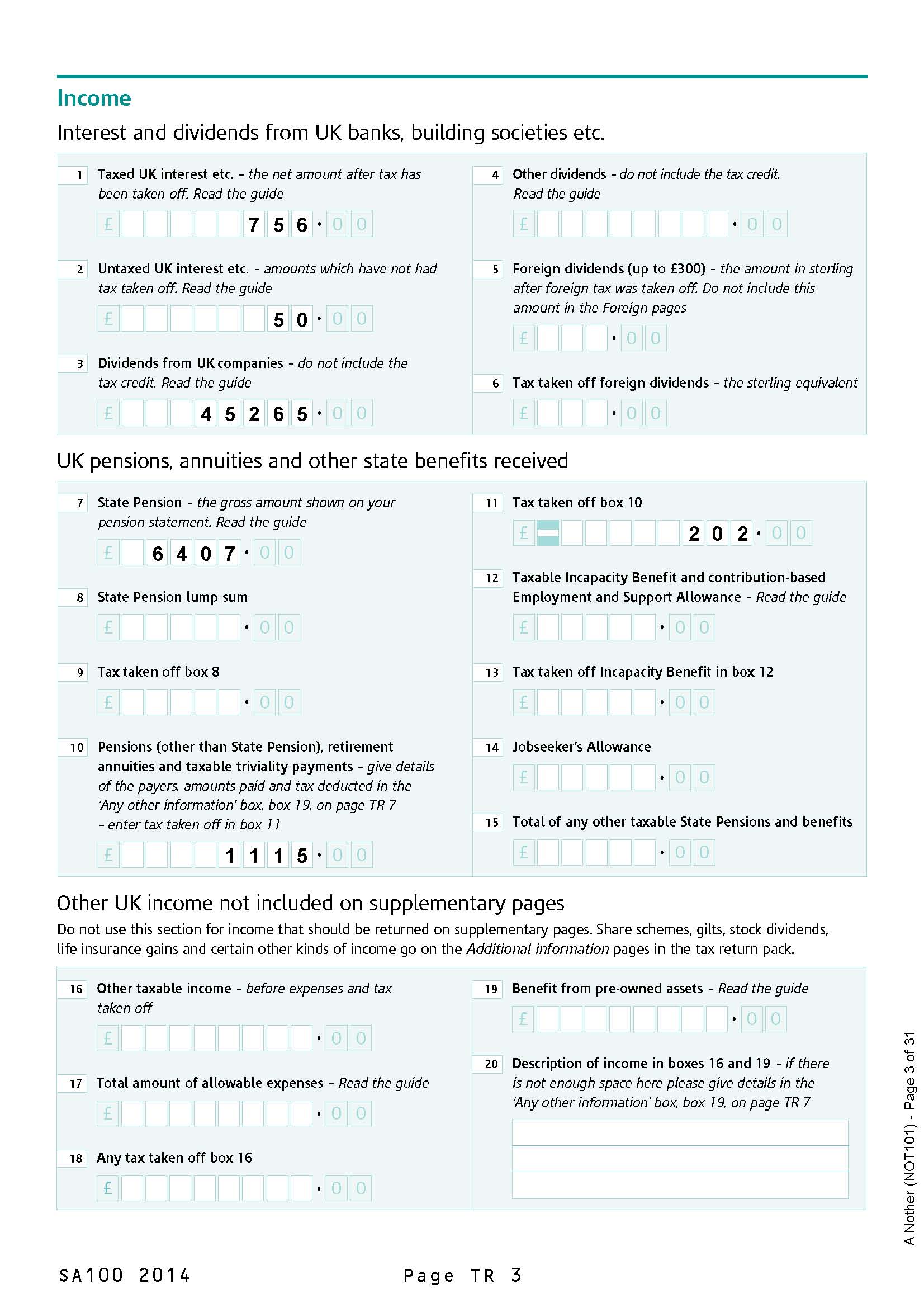

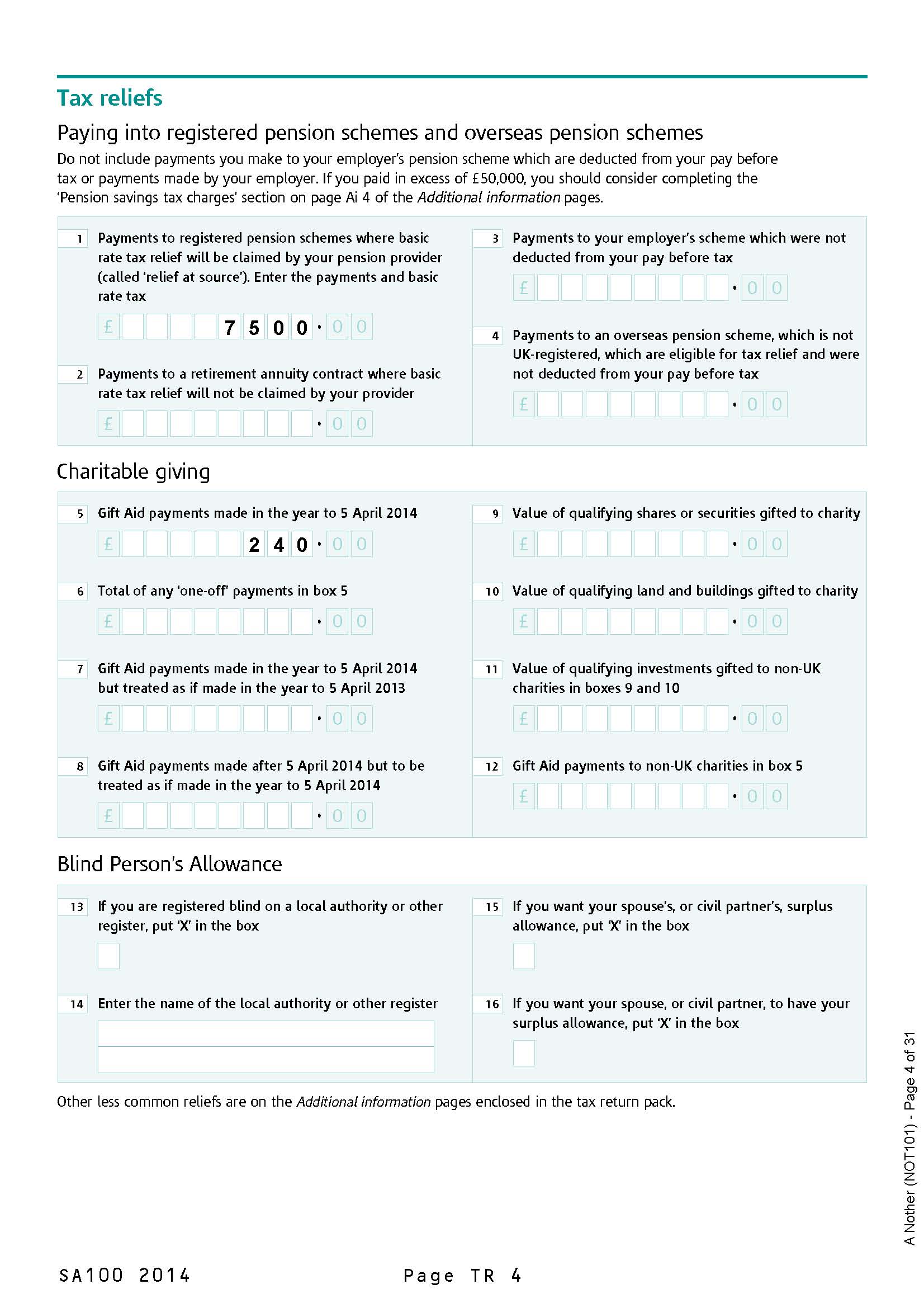

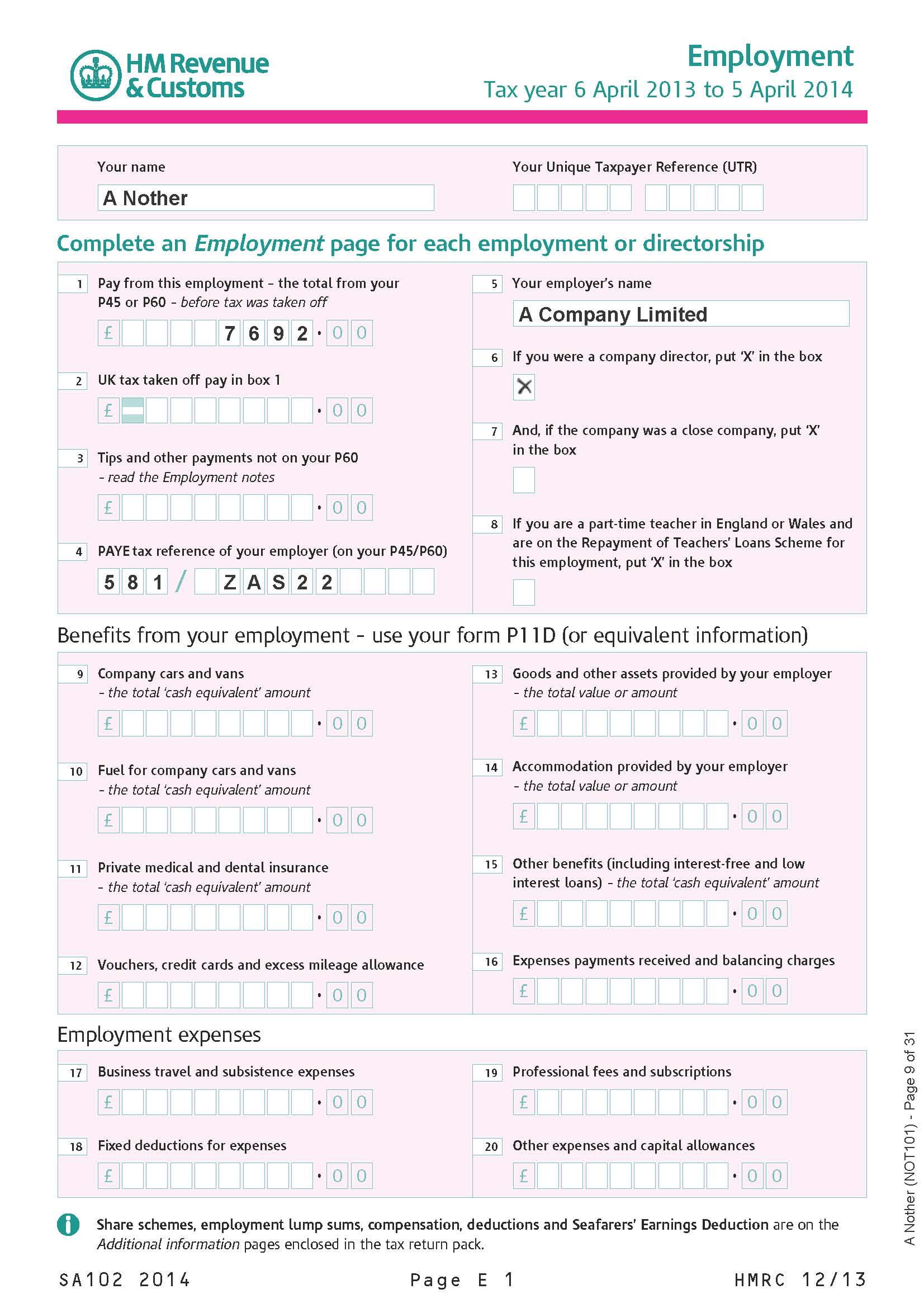

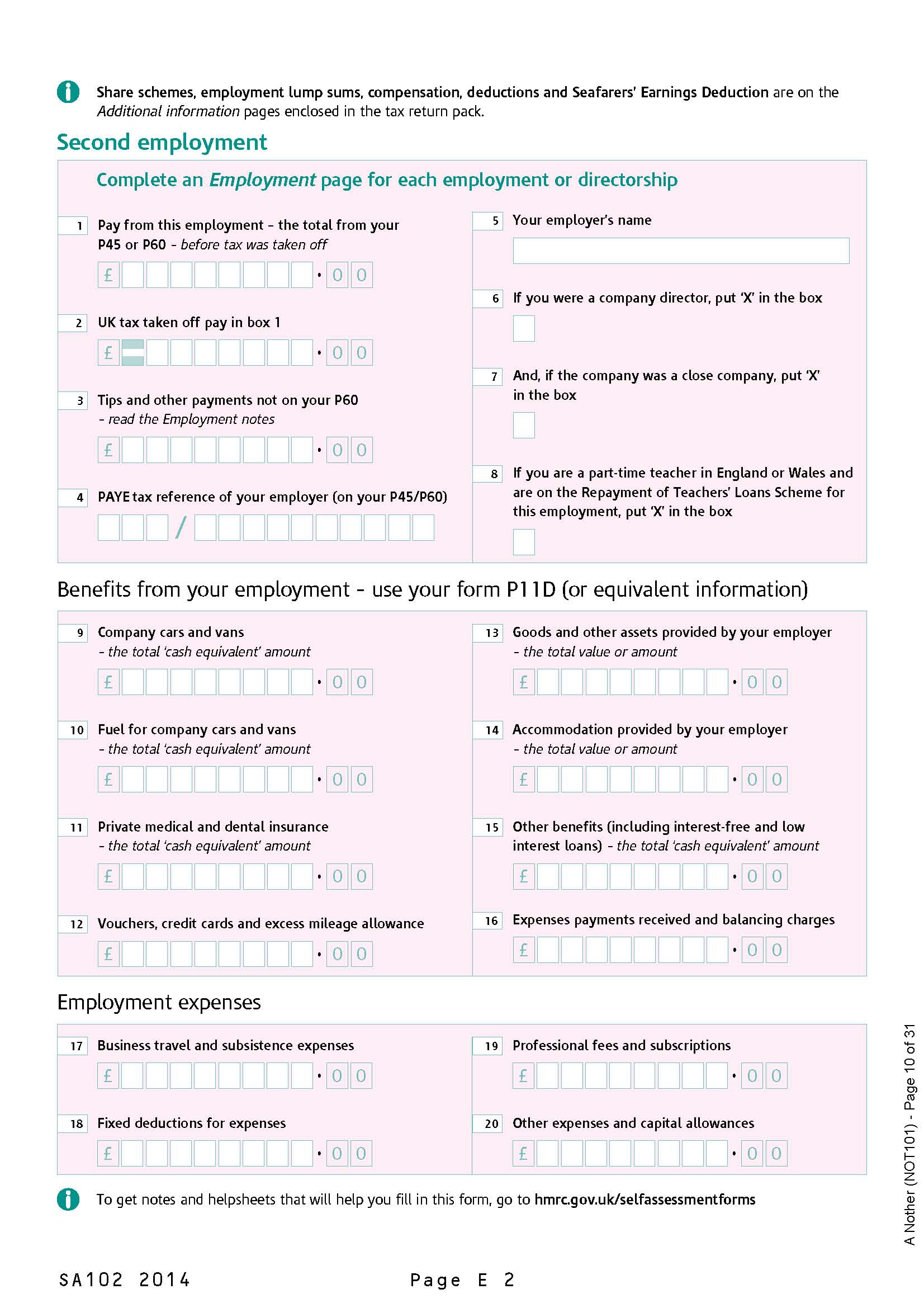

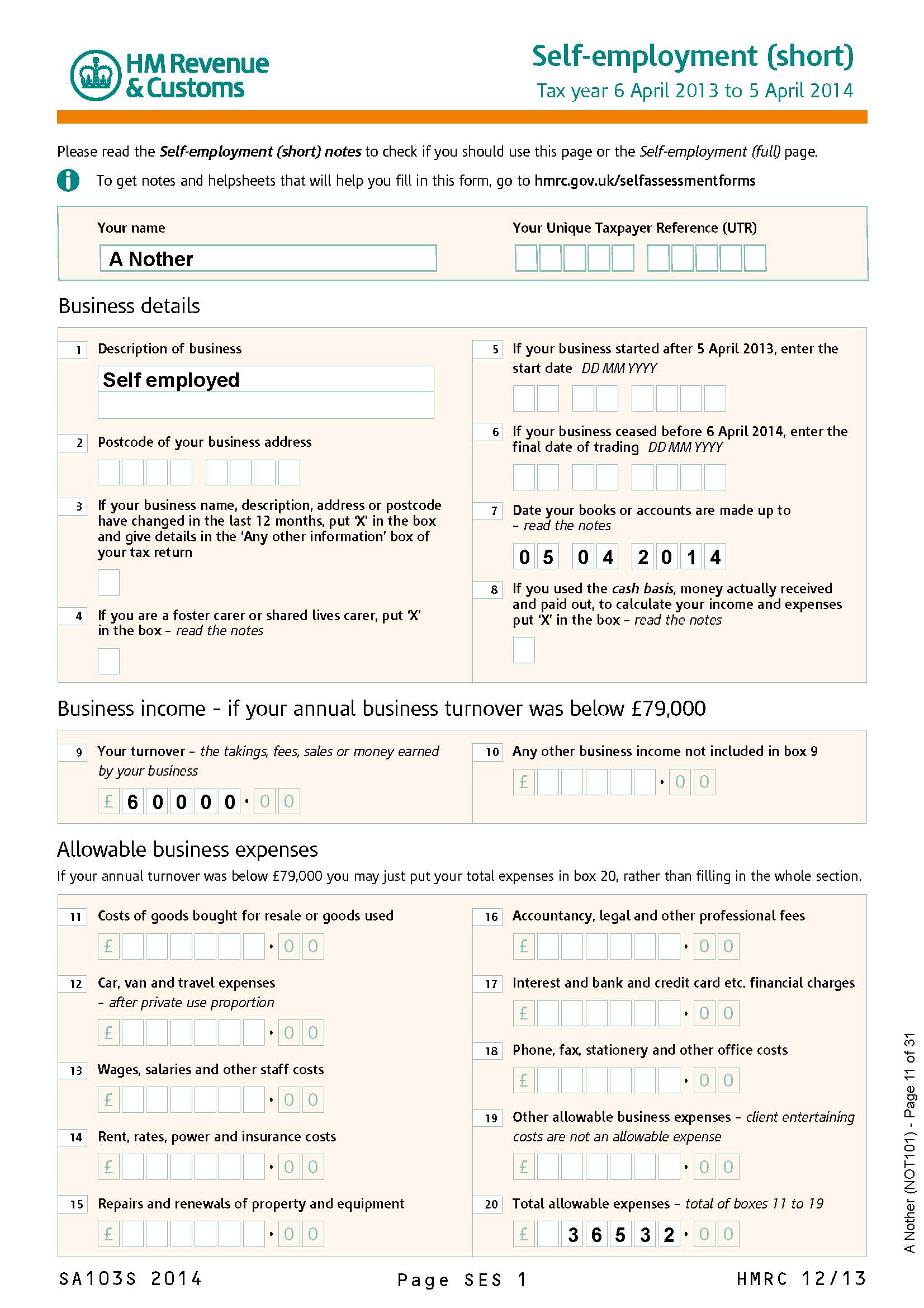

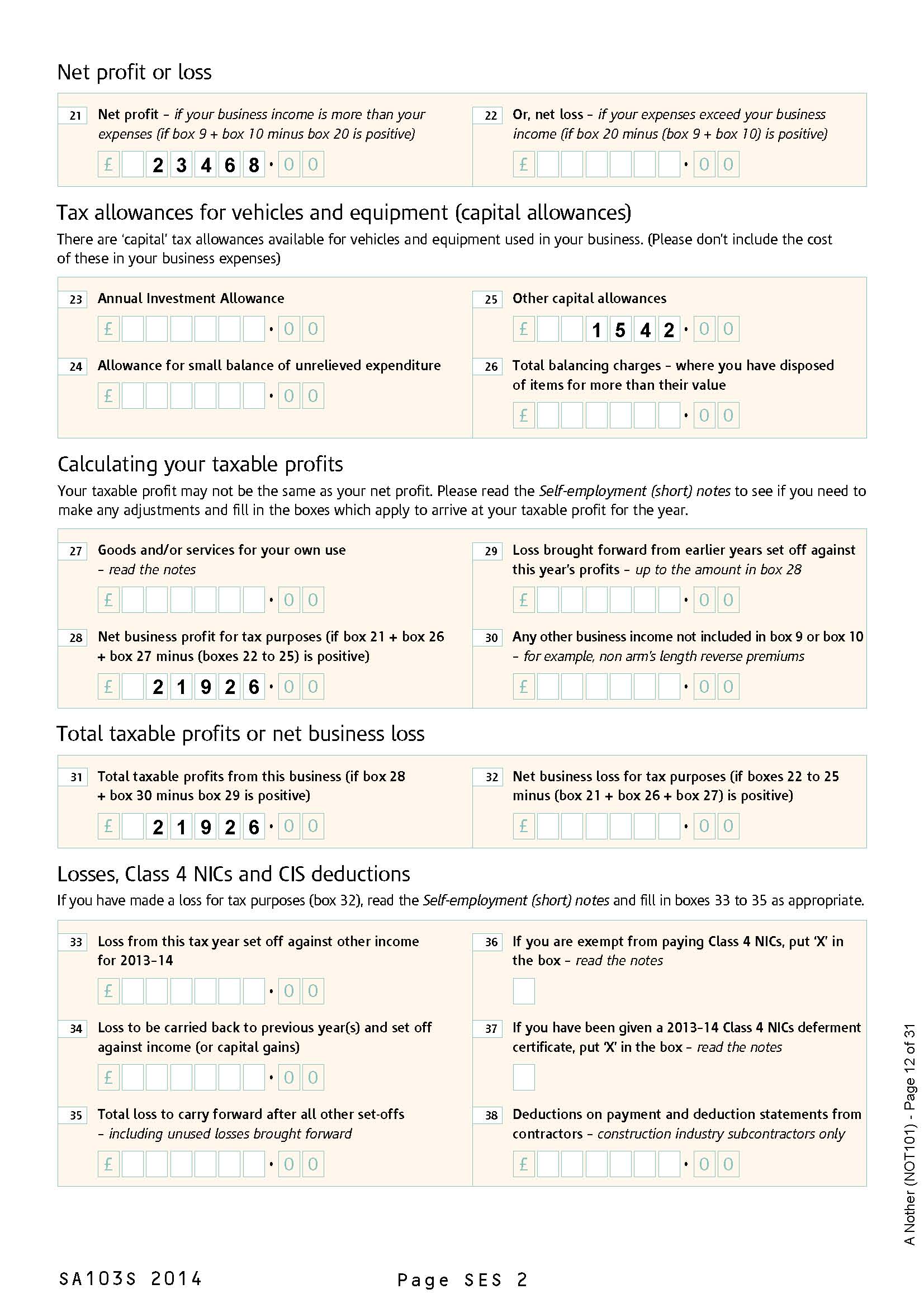

The basic Tax return (SA100) for Sole Traders includes the following*;

1) An evaluation which identifies any issues in your records which may affect your tax return and advice how to correct this.

2) Preparation of a basic SA100 Self Employed Sole Trader’s tax return to draft copy including;

a) SA100 TR1 questions 1 – 4 Your personal details

b) SA103 TR2 section 2* Self Employment income pages

c) SA100 TR7 questions 15 – 18 your tax advisor

d) SA100 TR8 questions 20 – 21 declaration

3) Your questions answered.

4) Amendments to your tax return

5) Final SA100 Self Assessment tax return ready for filing.

If you have more complicated tax affairs for example, if you have another employment, stocks and shares income, or are a landlord then you should bolt on to this purchase one of our additional products which will ensure that your tax affairs are properly stated.

*If you have more than one self employed business you will need to select the SA103 self employment bolt on product.

Simply provide us with the information we request and we will produce your SA100 tax return for you ready to file. You will be able to ask your Helpbox chartered accountant questions.

Who are HMRC?

Her Majesties Revenue and Customs (HMRC) are responsible for

collection of all taxes in the UK, commonly known as the ‘Taxman’.

How to Register

as an employer with HMRC

An employer has a need to register the business with Her

Majesties Revenue and customs HMRC, commonly known as the ‘Taxman’.

Dealing with HMRC and

paying tax

External functions include providing information

to Government agencies most commonly Her Majesties Revenue and Customs

Quickbooks

accountancy software

Provide us a back up of your Quickbooks software using the

Helpbox upload bay. We will then prepare your annual accounts from your

Quickbooks. Preparing annual accounts from Quickbooks via Helpbox is probably

the most affordable way to prepare your annual accounts.

A sole trader also known as sole proprietorship,

also more simply a proprietorship, is a type of business

entity that is owned and run by one person (individual). There is in

English Law no legal distinction between the business owner and the traded

business.

For example:

John Smith is an individual.

Let’s assume John is a qualified plumber and he sets up a

new business plumbing business start-up called “local plumbers”. This becomes

the trading style of the business. However, in law John Smith is the legal

entity so the sole trader business is John Smith trading as (sometimes

abbreviated to t/a) “Local Plumbers”. John

is responsible for all liabilities associated with the trading style “local

plumbers”. The full title of this sole trader is John Smith trading as Local

Plumbers.

The trading name is often used separately to the proprietors

individual name, in advertising etc. But all documentation should carry the

sole traders name somewhere on each business document.

The sole trader receives all profits (subject to HMRC

taxation which is declared on HMRC tax form SA100 also known as a personal self

assessment tax return). New start-up businesses should note that sole traders

have unlimited liability (responsibility) for all the businesses losses and

debts. Each of the business assets is owned by the Sole trader (proprietor) and

all debts of the business are the sole traders.

A very large proportion of business conducted in London and

the UK is undertaken by self employed sole traders working on their own.

Normally a sole trader will deal with the day-to-day record keeping and

administration (filings forms and paperwork). For more complicated record

keeping such as accountancy bookkeeping will involve the sole trader handing

over the business sales invoices and purchase receipts to an accountant who

will prepare the final end of year accounts and calculate the tax due.

The sole trader can open a bank account in their own name with their trading

style or without their trading style.

Advantages of becoming a sole

trader

It is the easiest business entity to start up a new

business. Organising your accounting records and complying with business law is

simpler than a partnership or a limited company.

Because the sole trader is responsible for all the business

debts sometimes banks and other lenders can be more willing to loan monies to

the business. The same goes for suppliers (creditors).

Unlike a limited company where the business is owned by the

company shareholders and the directors have legal responsibility under the

Companies Act 2006. Therefore they are restricted by that law on what income

they can receive from the limited company. A sole trader receives all the

profits from the business.

A common problem faced by new start up partnerships and

limited companies is that the more partners and directors the more chance that

you might fall out. Which often leads to business failure. A sole trader is a

simple entity where the proprietor makes all the decisions.

Disadvantages of

being a sole trader is that as the business becomes successful, the associated

business risks increase. To mitigate

those risks sole traders often incorporate. That is they form a limited

liability company

Sole trader Annual

Accounts

Sole traders have no

legal requirement to file accounts. However, HMRC say: If you have to send HMRC a tax

return, the law says that you must keep all the records and documents you need

to complete the return. If you don't have adequate records or if you don't keep

them for long enough, you may have to pay penalties.

Therefore, if an HMRC investigation is to be avoided proper

financial records have to be kept. These includes annual accounts.

Annual accounts are particularly helpful when completing the

self employed self assessment tax return (SA100).

Do sole traders have

to prepare the same annual accounts as limited companies?

year-end sole trader accounts are prepared in a shorter format than limited

company year-end financial statements. Because partnership year-end accounts

include a summary for each partner they are a little more complex than sole

traders. How much more complicated depends upon the number of partners in the

partnership.

Affordable

accountancy solutions for sole traders. This product is ideal for self employed

sole traders who want have the time and ability to book keep all their business

transactions onto an accountancy software programme. These include cloud based

online accountancy software as well as the traditional double entry models

including Sage, Quickbooks, Xero, Kashflow, Excel, Freeagent, Clearbooks and

Mybooks to enter their own bookkeeping records. If you are a self employed sole

trader and want to take advantage of

being your own bookkeeper. Then when you enter details of your business

transactions, purchase receipts, sales invoices and bank statements, and any

payroll wages you have run or HMRC PAYE, you have a better understanding of the

actual performance of your business. A second advantage is that having spent

time bookkeeping your business transactions you have saved the cost of paying a

bookkeeper to account for those transactions. Our online and cloud based

software filing master saves you both time and money, and maximises your

efforts. The gains go into your pocket rather than the pocket of another

accountant or accountancy firm. From

your own bookkeeping software we will prepare a set of year end accounts,

including profit and loss schedule and balance sheet. Whether you are VAT

registered or not, a new start-up or existing business, we will provide a

seamless service which includes preparing HMRC ready annual accounts. Which

means we can also provide a very affordable tax filing service from those year

end annual accounts. Excellent product for the self employed sole trader

business.

What

is a self employed person?

The UK Government is keen for more people to set up in business a

self-employed. One of the key attractions for becoming self employed is that

you no longer have to work for someone else. You are your own boss. Being your

own boss requires new start up business owner to be responsible for their own

sick pay, and paying your own taxes and pension provision.

What

is a self employed business entity?

Once you have decided to take the plunge and you start up your own new

business then you need to consider what kind of entity will operate your

business. Sole trader, partnership, or a limited liability company.

Registering as self employed with HMRC

start-up businesses choose simple self employment and trade their new business

as a sole trader. Whatever entity you choose you must register that you are

self employed with Her majesties Revenue & Customs HMRC. As well as

registering online with HMRC for self assessment tax returns. You should also

consider how you will pay your National Insurance contributions NIC’s

Partnership Tax

return (SA800)

Who has to submit a

self assessment tax return?

Each partnership should nominate a managing partner. That is

the partner who will take responsibility to manage the financial affairs of the

business. In law a partners in a partnership are subject to joint and several

liability. That means each and every partner is potentially personally liable

for all of the partnerships debts not just their own share. Often the managing

partner is the one who co-ordinates with us to provide the information need to

complete the year-end partnership (SA800) tax return form.

When does the tax

return have to be filed?

Each year the partnership must file with HMRC a partnership

tax return for all accounting transaction in the period 6th April to

5th April the following year. The SA800 partnership tax return must be

filed with HMRC no later than 31st January the following year.

declared on the self assessment tax return. Which must be paid in full. Any

late payments will be subject to surcharge penalty by HMRC. Likewise severe

penalties apply to late or non-submissions. These fines escalate very quickly

and within a few short weeks can exceed £1000.

Partners additional

tax returns

Anyone who is part of a business partnership, as the same

duty as a sole trader and must register their self employment with HMRC within

90 days of starting trading. Failure to

do so can result in HMRC fines and penalties. The partnership has to file a tax

return and additionally each partner must submit their own (SA100) self assessment

tax return.

Everyone who as a full time or part time income has to tell

Her Majesties Revenue and customs HMRC, commonly known as the ‘Taxman’, what

tax is due to the UK Governments exchequer.

Self employed people do this by filing an HMRC tax form

called a Self Assessment Tax return and is given the file name SA100. Its not

just self employed people who have to file a HMRC SA100 Tax return. Other

employed people including directors of limited liability companies, higher rate

tax payers, if you have a separate part-time income from self employment, such

as income from renting property, some kinds of pensions and stocks and shares.

Partners in a business Partnership are self employed and

must register with HMRC and file a SA100 self assessment tax return each year.

The tax return has to be filed each year before 31stJanuary and any income relating to the previous years income between 6th April and the

following 5th April. For example:

On the 31st January 2016 HMRC self assessment tax

return you have to account for income relating to the period 6thApril 2014 until 5th April 2015.

It is important to employ a tax accountant to prepare a set

of year end annual accounts profit and loss schedule for the relevant tax

period. A self employed person such as a sole trader or a partner in a business

partnership is allowed to offset their business expenses against their income.

Including purchase receipts which are verified by bank statements helps reduce

the profit and as a consequence reduce the amount of tax payable to HMRC.

It is very important to understand the UK HMRC

tax rules because if the HMRC tax rules say you should register for self

assessment tax assessment, and file an HMRC SA100. If you do not file a tax

return then you are liable to sever, fines and penalties, which will be imposed

on you by HMRC. In more serious cases where the taxpayers is considered to have

ignored their duty to register with HMRC for the purposes of declaring their income,

can face criminal charges which carry penalties of fines and imprisonment.

Every company has each year to comply with the Companies Act

2006 and file an annual return at companies house. Not to do so is a criminal

offence and convicted directors are liable to pay a fine and have a criminal

record registered against their individual names.

Also every newly

incorporated company must register the new limited liability company with HMRC

for purposes of being assessed for payment of corporation tax.

Thereafter each year the Ltd Co., must file with Her

Majesties Revenue and customs HMRC, commonly known as the ‘Taxman’, a

corporation tax return. This HMRC form has a form name CT600.

It is very important to understand the UK HMRC

tax rules because every limited liability company must register and file an

HMRC CT600. If you do not file a tax return then you are liable to sever, fines

and penalties, which will be imposed on you by HMRC. In more serious cases where

the company is considered to have ignored their duty to register with HMRC for

the purposes of declaring income. The directors can face criminal charges which

carry penalties of fines and imprisonment.

Company directors should be aware of their obligation to

register their directorship with HMRC so that they can have their income

assessed for possible taxation.

Everyone who as a full time or part time income has to tell

Her Majesties Revenue and customs HMRC, commonly known as the ‘Taxman’, what

tax is due to the UK Governments exchequer.

Self employed people do this by filing an HMRC tax form

called a Self Assessment Tax return and is given the file name SA100. Its not

just self employed people who have to file a HMRC SA100 Tax return. Other

employed people including directors of limited liability companies, higher rate

tax payers, if you have a separate part-time income from self employment, such

as income from renting property, some kinds of pensions and stocks and shares.

The tax return has to be filed each year before 31stJanuary and any income relating to the previous years income between 6th April and the

following 5th April. For example:

On the 31st January 2016 HMRC self assessment tax

return you have to account for income relating to the period 6thApril 2014 until 5th April 2015.

It is important to employ a tax accountant to prepare a set

of year end annual accounts profit and loss schedule for the relevant tax

period. A self employed person such as a sole trader or a partner in a business

partnership is allowed to offset their business expenses against their income.

Including purchase receipts which are verified by bank statements helps reduce

the profit and as a consequence reduce the amount of tax payable to HMRC.

It is very important to understand the UK HMRC

tax rules because if the HMRC tax rules say you should register for self

assessment tax assessment, and file an HMRC SA100. If you do not file a tax

return then you are liable to sever, fines and penalties, which will be imposed

on you by HMRC. In more serious cases where the taxpayers is considered to have

ignored their duty to register with HMRC for the purposes of declaring their income,

can face criminal charges which carry penalties of fines and imprisonment.

Every company has each year to comply with the Companies Act

2006 and file an annual return at companies house. Not to do so is a criminal

offence and convicted directors are liable to pay a fine and have a criminal

record registered against their individual names.

Also every newly

incorporated company must register the new limited liability company with HMRC

for purposes of being assessed for payment of corporation tax.

Thereafter each year the Ltd Co., must file with

Her Majesties Revenue and customs HMRC, commonly known as the ‘Taxman’, a

corporation tax return.

This HMRC form has a form name CT600.

It is very important to understand the UK HMRC

tax rules because every limited liability company must register and file an

HMRC CT600. If you do not file a tax return then you are liable to sever, fines

and penalties, which will be imposed on you by HMRC. In more serious cases

where the company is considered to have ignored their duty to register with

HMRC for the purposes of declaring income. The directors can face criminal

charges which carry penalties of fines and imprisonment.

What happens if I

don’t file a Tax return?

HMRC have very powerful and wide ranging powers including

the power of arrest. If you fail to either register and or file a tax return,

then HMRC powers allow then to impose financial penalties and charge interest

on any due tax.

What

is a self employed person?

The UK Government is keen for more people to set up in business a

self-employed. One of the key attractions for becoming self employed is that

you no longer have to work for someone else. You are your own boss. Being your

own boss requires new start up business owner to be responsible for their own

sick pay, and paying your own taxes and pension provision.

What

is a self employed business entity?

Once you have decided to take the plunge and you start up your own new

business then you need to consider what kind of entity will operate your

business. Sole trader, partnership, or a limited liability company.

Registering as self employed with HMRC

start-up businesses choose simple self employment and trade their new business

as a sole trader. Whatever entity you choose you must register that you are

self employed with Her majesties Revenue & Customs HMRC. As well as

registering online with HMRC for self assessment tax returns. You should also

consider how you will pay your National Insurance contributions NIC’s

Everyone who as a full time or part time income has to tell

Her Majesties Revenue and customs HMRC, commonly known as the ‘Taxman’, what

tax is due to the UK Governments exchequer.

Self employed people do this by filing an HMRC tax form

called a Self Assessment Tax return and is given the file name SA100. Its not

just self employed people who have to file a HMRC SA100 Tax return. Other

employed people including directors of limited liability companies, higher rate

tax payers, if you have a separate part-time income from self employment, such

as income from renting property, some kinds of pensions and stocks and shares.

Partners in a business Partnership are self employed and

must register with HMRC and file a SA100 self assessment tax return each year.

The tax return has to be filed each year before 31stJanuary and any income relating to the previous years income between 6th April and the

following 5th April. For example:

On the 31st January 2016 HMRC self assessment tax

return you have to account for income relating to the period 6thApril 2014 until 5th April 2015.

It is important to employ a tax accountant to prepare a set

of year end annual accounts profit and loss schedule for the relevant tax

period. A self employed person such as a sole trader or a partner in a business

partnership is allowed to offset their business expenses against their income.

Including purchase receipts which are verified by bank statements helps reduce

the profit and as a consequence reduce the amount of tax payable to HMRC.

It is very important to understand the UK HMRC

tax rules because if the HMRC tax rules say you should register for self

assessment tax assessment, and file an HMRC SA100. If you do not file a tax

return then you are liable to sever, fines and penalties, which will be imposed

on you by HMRC. In more serious cases where the taxpayers is considered to have

ignored their duty to register with HMRC for the purposes of declaring their income,

can face criminal charges which carry penalties of fines and imprisonment.

Company directors should be aware of their obligation to

register their directorship with HMRC so that they can have their income

assessed for possible taxation.

Everyone who as a full time or part time income has to tell

Her Majesties Revenue and customs HMRC, commonly known as the ‘Taxman’, what

tax is due to the UK Governments exchequer.

Self employed people do this by filing an HMRC tax form

called a Self Assessment Tax return and is given the file name SA100. Its not

just self employed people who have to file a HMRC SA100 Tax return. Other

employed people including directors of limited liability companies, higher rate

tax payers, if you have a separate part-time income from self employment, such

as income from renting property, some kinds of pensions and stocks and shares.

The tax return has to be filed each year before 31stJanuary and any income relating to the previous years income between 6th April and the

following 5th April. For example:

On the 31st January 2016 HMRC self assessment tax

return you have to account for income relating to the period 6thApril 2014 until 5th April 2015.

It is important to employ a tax accountant to prepare a set

of year end annual accounts profit and loss schedule for the relevant tax

period. A self employed person such as a sole trader or a partner in a business

partnership is allowed to offset their business expenses against their income.

Including purchase receipts which are verified by bank statements helps reduce

the profit and as a consequence reduce the amount of tax payable to HMRC.

It is very important to understand the UK HMRC

tax rules because if the HMRC tax rules say you should register for self

assessment tax assessment, and file an HMRC SA100. If you do not file a tax

return then you are liable to sever, fines and penalties, which will be imposed

on you by HMRC. In more serious cases where the taxpayers is considered to have

ignored their duty to register with HMRC for the purposes of declaring their income,

can face criminal charges which carry penalties of fines and imprisonment.